Finding Value

posted on

Feb 17, 2009 03:09AM

Brazil, Argentina, Chile, Mexico - Yamana is targeting sustainable gold production of 2.2 M oz of gold by 2012.

Yamana Gold (NYSE: AUY) is a difficult company to follow. It seems that as soon as you get a handle on the business, something changes. I originally bought the company thinking of it as a simple business: Pull gold out of the ground, sell it and then profit, but it’s not that simple.

Yamana Gold (NYSE: AUY) is a difficult company to follow. It seems that as soon as you get a handle on the business, something changes. I originally bought the company thinking of it as a simple business: Pull gold out of the ground, sell it and then profit, but it’s not that simple.

One of the factors that must be considered regarding Yamana is the cost of developing new mines. Yamana has grown gold production dramatically in just the past few years, and it has done this through new mine development and acquisition. Despite this new production, it is still difficult to tell if there has been value created for shareholders.

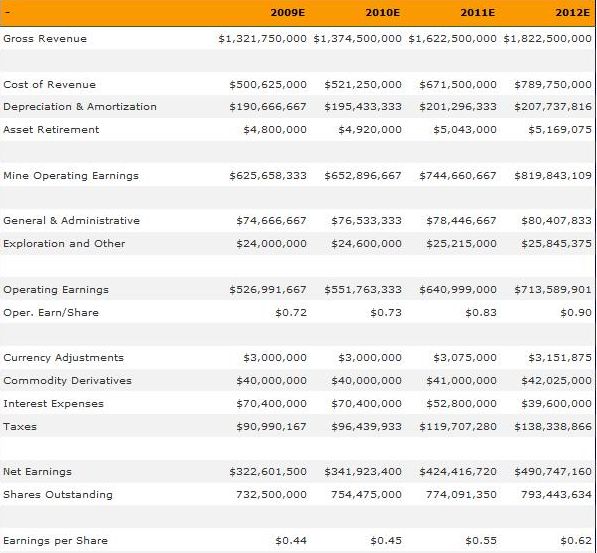

Yamana has financed the majority of its development and acquisitions with share issuances. Any “win” on the side of development has been almost entirely offset by share dilution. Going forward, Yamana will have to continue this practice as debt financing has grown increasingly difficult. The company has set a production goal of 2 million gold equivalent ounces by 2012. It has also indicated that 2009 production should be in the range of 1.3-1.4 million gold equivalent ounces, while 2010 should be in the range of 1.4-1.5 million ounces. Based on these goals and its indicated costs of production, I’ve tried to create a forward-looking income statement.

click on charts to enlarge

Revenue

Revenue is based on the lower range of gold equivalent ounce production along with the minimum range of copper production at the Chapada mine. This revenue figure is based on gold at $800 per ounce. Copper is estimated at $1.75 per pound.

Cost of Revenue

Cost of Revenue is based on the upper end of Yamana’s projected range at $375 per gold equivalent ounce. This cost grows to $395 in 2011 and to $405 in 2012.

General & Administrative

I assume some expense control in General and Administrative expenses. Based on the recent acquisitions, there are likely some cost savings to be obtained here, so I haven’t projected these expenses to grow as fast as revenues.

Hedging

It is rather difficult to estimate how the hedging costs will work out. I have kept this fairly consistent with its 2008 experience.

Cash Flow

As part of the cash flow portion of this model, I’ve added back Depreciation and Amortization and then subtracted sustaining capex as noted in the company’s most recent press release concerning its 2009 and 2010, outlook.

Shares Outstanding and Development Requirements

I’ve kept the cash balance relatively consistent, and estimated that Yamana will continue to issue shares to fund mine development costs. Based on the previously noted assumptions, there is incremental value to shareholders. Assuming a P/CF of about 22, the share price would be about $15 in 2012.

Sensitivity and the Price of Gold

This model is based on the price of gold staying around $800. As I wrote this, it was hovering around $950. If the price of gold rises to $1,000 per ounce in 2012, its cash flow would be $1.00 per share. If it falls to $650, then its cash flow would fall to around $0.40 per share.

Conclusion

Despite the difficulties in projecting forward earnings, I believe that holding Yamana does make sense in order to gain exposure to gold prices. As the world economy continues to struggle, the price of gold should remain high. It seems that the more uncertainty there is, the higher the price of gold climbs. Yamana’s production increases continue to serve as a kind of hedge against falling gold prices - up to a point. However, if gold falls below $650, returns would definitely suffer.

Disclosure: I currently hold shares of Yamana Gold.