Stocks: Why One More Major Correction Still Lies Ahead

posted on

May 29, 2012 12:43PM

Edit this title from the Fast Facts Section

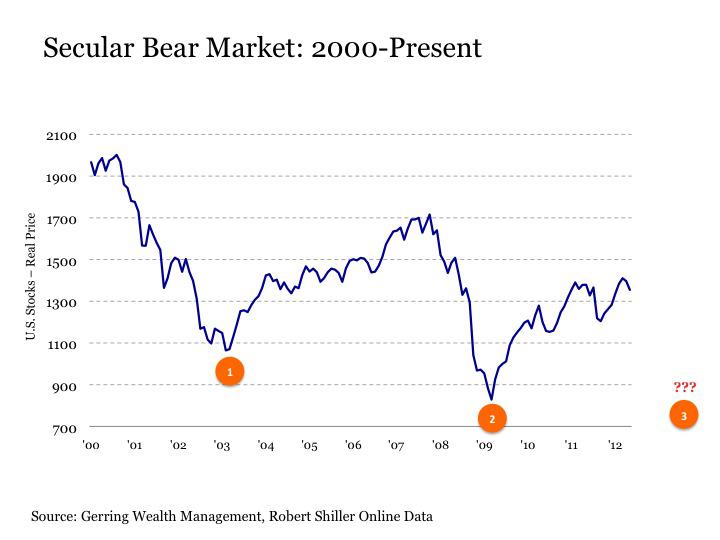

It is said that bad things come in threes. A case where this is explicitly true is when it comes to secular bear markets for stocks. History has shown that when stocks enter such periods of prolonged decline that three major corrections occur before a new secular bull market begins. And to date in the current secular bear market that began in 2000, we have only experienced two sharp declines. Thus, history suggests that one more major stock market correction still lies ahead before we reach the dawn of a new sustained rise in stocks.

It is said that bad things come in threes. A case where this is explicitly true is when it comes to secular bear markets for stocks. History has shown that when stocks enter such periods of prolonged decline that three major corrections occur before a new secular bull market begins. And to date in the current secular bear market that began in 2000, we have only experienced two sharp declines. Thus, history suggests that one more major stock market correction still lies ahead before we reach the dawn of a new sustained rise in stocks.

Dating back to the Buttonwood Agreement in 1792, U.S. stocks have experienced prolonged secular bull markets periods of steady gains followed by similarly extensive secular bear market phases of choppy declines. These bear phases occur to cleanse the excesses that were built up in the market system from the prior bull cycle and have historically lasted 17 years on average.

A look back at history reveals a secular bear phase in stocks includes three major corrections. In some instances, these corrections are swift and staggering. In other instances these declines are slow and grinding. But regardless of their characteristics, they result in a distinctively trying experience for stock investors.

In evaluating past secular bear markets, it is important to view these phases on a real basis. This is due to the fact that periods of pricing instability can greatly distort true stock market results. For example, stock returns during a period of high inflation may appear stronger on a nominal basis before adjusting for inflation. Conversely, stock performance during periods of prolonged deflation may seem weaker on a nominal basis.

The following charts show the inflation-adjusted price performance of the stock market during the four previous secular bear markets over the past 150 years.

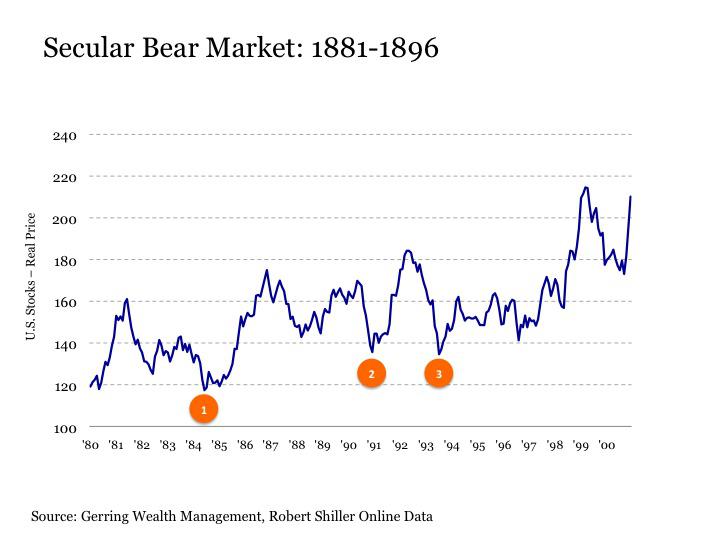

The first is the secular bear market from 1881 to 1896. The performance of the stock market actually appears firmer on a real basis, as it declined by over -40% on a nominal basis during this deflationary phase. During this period, the stock market experienced three major declines, which are shown in the chart below. Depending on how the data is dissected, it could be argued that as many as five major corrections occurred during this period.

The second is the secular bear market from 1901 to 1920. Unlike the previous secular bear market episode, while the nominal price performance of the market appears choppy but generally sideways during this period, the real returns on the market were considerably worse due to the massive inflation that occurred in and around World War I.

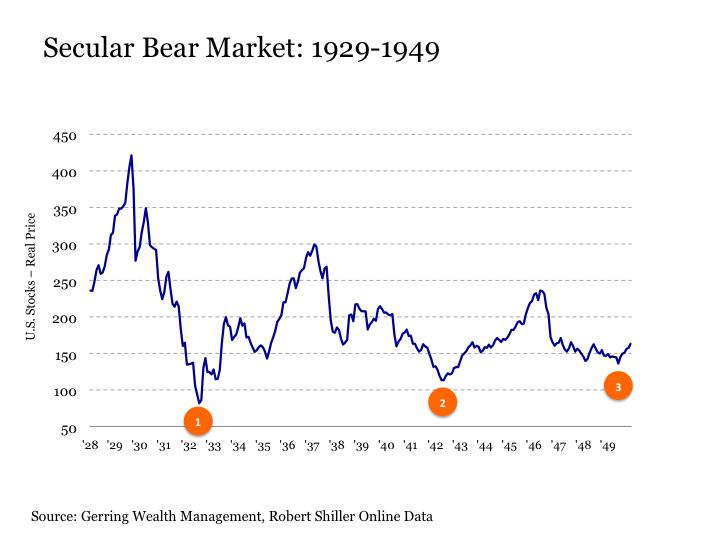

The third secular bear episode is perhaps the most notorious from 1929 to 1949, which of course included the deflationary Great Depression, World War II and it’s immediate inflationary aftermath. It could be argued that a fourth major correction occurred in 1938, although markets hardly bounced and continued to slide lower for the next several years before finally reaching the second bottom in 1942.

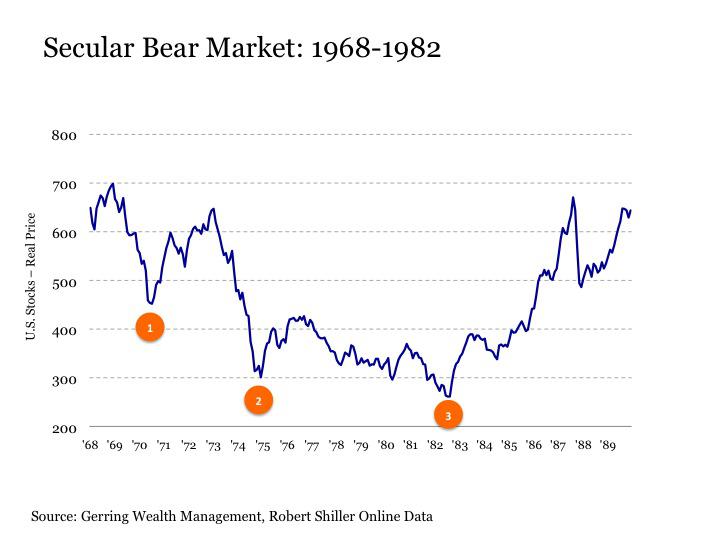

The fourth secular bear market from 1968 to 1982 was marked by a period of massive inflation. As a result, while it appears that the stock market simply chopped sideways on a nominal basis over much of this period, it actually dropped precipitously on a real basis.

Of course, the latest secular bear market began in 2000. And twelve years later, it is still unfolding. Several characteristics of the current secular bear market are notable at this point in time. First, at 12 years and counting, it is still shorter in duration by three years versus the previous shortest secular bear market in U.S. history at 15 years. But more importantly, we have experienced only two major corrections to this point. This implies that in order to follow historical precedent, one more major stock wash out lies ahead.

Perhaps it will be different this time and stocks will need to endure only two major corrections before catapulting into a new secular bull market. While this is certainly possible, I am always reluctant to make the statement that this time is different.

A variety of reasons support the conclusion that one more correction lies ahead in the current cycle. First, the downward sloping trend line resistance on a real basis remains firmly intact. Second, the economy and markets continue to cling to many of the excesses that remain from the previous secular bull market instead of allowing them to fully flush out. Lastly, one does not need to look far around the world to see where the next crisis catalysts might emerge. More specifically, the situation in Europe could disintegrate into crisis at any moment.

The stock market likely has one more major correction ahead. But the arrival of this correction may be a good thing, for it will likely be caused by the fact that the global economy has been finally forced to take its medicine and cleanse itself of its past excesses once and for all. Hopefully this cleansing can be carried out in a reasonably orderly way. Regardless, once this process is complete, we can finally begin looking forward to the dawn of a new secular bull market.

Disclaimer: This post is for information purposes only. There are risks involved with investing including loss of principal. Gerring Wealth Management (GWM) makes no explicit or implicit guarantee with respect to performance or the outcome of any investment or projections made by GWM. There is no guarantee that the goals of the strategies discussed by GWM will be met.