Extend and Pretend: Lessons From the Flash Crash

posted on

Jun 02, 2010 09:44AM

Edit this title from the Fast Facts Section

http://seekingalpha.com/article/208054-extend-and-pretend-lessons-from-the-flash-crash

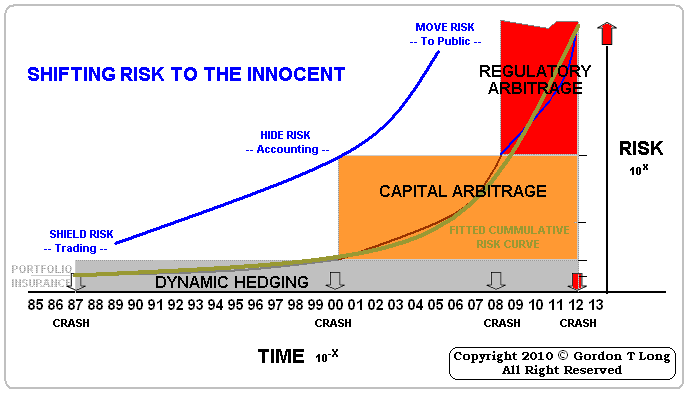

Reduces Risk further through recent advancements in High Frequency Trading and Dark Pools Hides Risk by removing it from financial balance sheets Moves Risk to Sovereign entities. Messages of the Flash Crash: Dynamic Hedging and Portfolio Insurance are both based on trend following mechanics. Consequentially both have a strong bias towards momentum correlation and the ability to adjust to changes in momentum. One of three flaws in most mathematical algorithms is the assumption of market liquidity. When markets breakdown, liquidity quickly evaporates and this often makes execution impossible. The more serious the breakdown the more serious the liquidity problem will become. Also, the liquidity issue is often simultaneously seen across multiple markets where modern dynamic hedging operates. The Flash Crash confirmed that Dynamic Hedging has now been modified by major players to take this into account and it is why the algorithms ‘grabbed’ as much liquidity as fast as it could, at accelerating rates, while liquidity was still available. The employment of High Frequency Trading has now emerged as a strategic imperative within state-of-the-art Dynamic Hedging Systems. A second flaw of trading algorithms and markets is counter party risk or the sudden failure of a counterparty to delivery a contracted obligation. With banks & financial institutions still having serious amounts of off balance sheet risk tied to Structured Investment Vehicles (SIVs) and corporations to Special Purpose Entities (SPEs) the ability to rapidly shift hedging on any indications are now paramount. Shifts in LIBOR, TED Spread, and OIS-Swap spread must now be acted upon in milliseconds. The Flash Crash occurred when all these input drivers were moving as a result of the euro crisis. Sovereign Debt Changes in Sovereign Debt Ratings have a profound impact on Collateral Calls associated with the $430 Trillion Interest Rate Swap market. Collateral Calls are typically tied to Credit Ratings, LIBOR, Spreads and Asset Values. Hedge positions on Trillion Dollar portfolios must now be repositioned in minutes versus days or even hours while liquidity and price is available. A third flaw of trading algorithms is their assumption of ‘continuity’ or continuously operating markets. Instability of any system can lead to compounding results or exponential change until the function reaches a point of discontinuity. We are witnessing higher amplitudes, shorter frequencies and steeper rates of change which are signs of instability in the market. As much as the market became fixated on the Flash Crash, what has received little attention are the dramatic “Flash Dashes” where markets on close for example are seeing 20 handles on the S&P. To long term traders these are worrying tell tales. To others they are evidence of accelerating & compounding Dynamic Hedging issue.

The recent Flash Crash is an omen of what lies ahead for the financial markets. It was a uniquely different occurrence than anything we have ever witnessed. Likewise, what we are about to experience will be unexpected and never before experienced by this generation.

Prior to the May 6th Flash Crash I laid out in an article “Extend & Pretend: Shifting Risk to the Innocent” what to expect. The ink was barely wet before its predictions began to rapidly unfold. The basis for the predictions was the similarities between the rally we have experienced since March 2009 and the rally prior to the 1987 crash. It was striking in comparison to the amount of rise, the rate and the pattern, but more importantly the reason for both rallies. The 1987 crash was attributed to Portfolio Insurance. In 2010 it is about what is referred to as the ‘son-of-portfolio insurance’ – Dynamic Hedging.

We have systematically shifted risk through the advancement of three new strategies that individually may seem sound but when pyramided as we have done over the last ten years set the stage for systemic instability.

For the full unabridged article: see Tipping Points

The three new strategies are:

Dynamic Hedging

Capital Arbitrage

Regulatory Arbitrage

I will not explore in this article how these strategies are being used and how they are building upon themselves (see “Extend & Pretend: Shifting Risk to the Innocent”) but rather I want to focus on what the Flash Crash has confirmed.Liquidity Driver

Counter Party Risk Driver

Instability

Conclusion:

Flash Crashes and Dashes will become more apparent. By their very nature they are de-stabilizing. When certain natural frequency boundary conditions are broken the markets will eventual seize up despite all circuit breakers and attempts by authorities to stabilize markets. These boundary conditions are not presently understood nor seen to exist. For practitioners of Chaos Theory, Fractals and Mandelbrot Generators they are a basic tenet to understanding any phase shift.

We are nearing a ‘phase shift’ in what I will refer to as the energy level of the markets. Elliott Wave practitioners would refer to it as a ‘higher degree pivot’. W D Gann practitioners would call it a Gann Cardinal. Economists call it a “Tipping Point”. I call it a ‘Critical Point’ or ‘Chaotic Transient’.

A trader would just call it a market melt-down or melt-up!

Disclosure: No Positons

About the author: Gordon Long