Rusoro Receives Preliminary Assessment for Choco 10

posted on

May 19, 2009 07:34AM

Unlocking One of the World’s Most Prolific Gold Mining Regions

| May 19, 2009 | ||

|

Rusoro Receives Preliminary Assessment for Choco 10

Production Expansion of Choco 10 shows potential to expand gold production to Over 500,000 oz/yr, with operating costs estimated to be in the world's lowest quartile and robust cash flows. |

||

|

VANCOUVER, BRITISH COLUMBIA--(Marketwire - May 19, 2009) - George Salamis, President of Rusoro Mining Ltd. ("Rusoro" the "Company") (TSX VENTURE:RML) is pleased to provide an overview of the results of a recently completed Preliminary Assessment (the "PA" or "the Study"). The PA, also known in the mining industry as a Scoping Study, conducted by Micon International Limited ("Micon") has examined a number of different gold production expansion scenarios sourcing gold resources and reserves from the Choco 10 mine (95% owned) and the near-by Increible 6 (100% owned) gold deposit. The objective of the study was to evaluate the potential for expansion of the project. In order to do this, the cash flow of the unexpanded (5,000 t/d) base case and each of three expansion options has been forecast, enabling a comparison to be made of the NPV of each option versus the base case. The gold processing parameters studied the construction of a new 10,000 t/d mill and two alternative 20,000 t/d mill cases: one involving a completely new mill and one studying the achievement of 20,000 t/d milling capacity using a combination of existing Choco 10 processing capacity run in parallel with newly constructed milling facilities on the same site. Results in this press release are presented for the optimal case (Case 2) which is comprised of the existing facility at 5,000 t/d plus an additional 15,000 t/d of new capacity. The mining scenarios envisaged in the study, examined both owner-operated mine haulage fleets and contract mining operations, with both aimed at open pit mining on the extensive resources on both concessions. Open pit shell optimizations used in the mine scheduling of estimated resources to be mined at both projects used a gold price of $US 700/oz. In summary, the results of the PA are highly encouraging and Rusoro remains committed to bringing the project to feasibility by Q2, 2010. The Study shows that over the first three years of production, an expanded Choco 10 Milling Complex will average 545,500 oz Au/yr from 7,300,000 t/yr treated at an average head grade of 2.58 g/t Au, with cash costs averaging $US 331/oz over the life-of-mine (LOM). Highlights and Conclusions The following highlights are taken from Case 2 of the PA comprised of the existing 5,000t/d processing facility plus an additional 15,000 t/d of new capacity. - Potential to increase existing steady-state production at Choco 10 to over 500,000 oz/yr over a 12 year mine life. - The most robust financial outcome of the PA is derived from combining existing hard-rock milling capacity at Choco 10 with a new 15,000 t/d mill construction, for a total capacity 20,000 t/d. - Contract mining generates better financial returns versus owner-operated mine fleet arrangements in the PA. - Gold production at the expanded mine and mill facility is forecasted to reach a maximum of over 717,300 oz in Year 10, with an average rate of 558,200 oz/yr, post expansion. - LOM cash cost estimate is $US 331/oz. - Expansion capital requirements estimated at $US 208.5 million plus contingencies of $US 30.8 million and sustaining capital of $US 80.3 million over the life of mine (12 years). - Life-of-mine net revenue of $US 3.57 billion using $US 700 Au. Average annual after-tax cash flow of $US 77 million at $US 700/oz Au, - Payback, post commissioning of the expanded plant, is estimated at 2.1 years (discounted at 8%), on a total mine-life of over 12 years. - At a gold price of $US 700/oz, the PA estimates the NPV (8%) to be $US 449.7 million and after-tax IRR of 51.7%. Using a gold price of $US 850/oz, the project generates an NPV (8%) of $US 741.9 million and an after-tax IRR of 120.7%. - Upside: The table below shows the project sensitivities and upside of the expansion to higher gold prices. Economic Sensitivity to Gold Price(i)

-------------------------------------

-------------------------------------

Au Price NPV8 IRR

-------------------------------------

-------------------------------------

450 (58,555) 3.7

500 50,624 12.0

550 154,075 20.8

600 254,075 20.8

650 352,208 40.1

700 449,768 51.7

750 547,318 66.3

800 644,646 86.3

850 741,975 120.7

900 839,304 N/A

950 936,633 N/A

-------------------------------------

-------------------------------------

(i) In the PA the forecast gold price

is quoted net of applicable taxes.

In May 2008, Rusoro commissioned Micon to provide an independently generated Preliminary Assessment, also commonly referred to as a Scoping Study, for the Choco 10 (95% owned) and Increible 6 (100% owned) gold deposits, situated in the El Callao District of Bolivar State, Venezuela. Rusoro purchased the Choco 10 mine from Gold Fields Ltd in November 2007, on the basis that production at the active gold mine could be substantially expanded due to the size and distribution of the gold resources underlying the concession. Also at the time of purchase, the Company's view of the production expansion potential of the Choco 10 mining and milling complex was further enhanced by the synergies borne from the proximal location of its 100% owned Increible 6 gold project, situated only 8 km from the Choco 10 mill. In the PA, the Choco 10 and Increible 6 deposits were designed as open-pit operations with a construction phase of approximately 2 years. With the current resource base of the two projects, the anticipated life of the expanded mine is 12 years with an optimal mill throughput shown to be 20,000 tonnes per day. Gold production averages 558,200 oz/yr, post expansion with an average total cash cost of $US 331/oz. Power and water services are readily available on site, as are roads and mine site infrastructure. Capital expenditures are estimated at $US 208.5 million including EPCM costs, plus $US 80.3 million of sustaining capital injected over the life of the mine, plus contingencies of $US 30.8 million, giving the project a capital expenditure per recoverable ounce of gold of $US 55.65. Mineral resources that are not mineral reserves do not have demonstrated economic viability. The preliminary assessment is preliminary in nature, and includes inferred mineral resources that are considered too speculative geologically to have economic considerations applied to them that would enable them to be categorized as mineral reserves, and there is no certainty that the preliminary assessment will be realized. Mining and Mineral Processing Feedstock for the expanded mill will be provided by mined output from the existing Choco 10 operation (comprising the presently operating Rosika, Coacia and Pisolita open pits) and planned mine production from the Villa Balazo-Karolina (VBK) pit at Choco 10 and from the Increible 6 concession which is located 4 km northeast of Choco 10 and from the small Capia and Cerro Azul deposits. The stripping ratio is estimated at 5.73 to 1 over the life of mine, with pit designs modeled at 40 degrees in saprolite and 47 degrees in hard-rock. Mining costs for waste rock and mill feed have been estimated at an average of $2.48/t mined, under the contract mining scenario. The study envisages that the Choco 10-Increible 6 ores will be processed by conventional means, consisting of primary crushing, two-stage milling, cyanide leaching, carbon adsorption and elution, electro-winning and gold smelting. The plant design is a conventional cyanidation and carbon in pulp plant with a nominal throughput capacity of 20,000 t/d (7.3 Mt/yr) based on a 90 to 92% plant availability, depending on ore type. Total gold recovery is expected to average 90% based on an average head grade of 2.72 g/t Au over the life of the mine for design criteria. It should be noted that the study envisages the using the same processing methodology, on an expanded basis, as is currently conducted at the Choco 10 site. The mineral processing costs for the 20,000 t/d case, including tailings operations and power, are estimated at $US 4.34/t milled. General and Administrative Operating costs are estimated to be $US 2.67/t, for the Case 2 20,000 t/d case. Study Parameters The objective of the study was to evaluate the potential for expansion of the project. In order to do this, the cash flow of the unexpanded (5,000 t/d) base case and each of three expansion options has been forecast, enabling a comparison to be made of the NPV of each option versus the base case. The expansion options considered have total plant throughputs of 10,000 t/d and 20,000 t/d, as follows: - Case 1: A new plant operating at 10,000 t/d - Case 2: The existing plant (5,000 t/d) plus a new plant at 15,000 t/d, for a total of 20,000 t/d - Case 3: A new plant with two new lines at 10,000 t/d each, for a total of 20,000 t/d. The analysis has been undertaken in United States constant dollars of January 2009 value, i.e., without provision for inflation. The PA base case valuation assumes a constant gold price of $US 700/oz over the full project life. Capital and operating costs have been estimated at an overall accuracy of +30%, which is considered appropriate for preliminary assessment of a mining project of this nature. As part of its sensitivity analysis, Micon tested a range of prices and costs 30% above and below the base case values. The table below show a summary of the life-of-mine (LOM) cash flow projections and economic results for each of the production rate scenarios considered in the study. LOM Cash Flow Projections ($ millions) - Using $US 700/oz gold

---------------------------------------------------------------------------

---------------------------------------------------------------------------

Item Base Case 2

Case Case 1 5,000 Case 3

5,000 10,000 +15,000 2x10,000

t/d t/d t/d t/d

---------------------------------------------------------------------------

---------------------------------------------------------------------------

Net Sales Revenue 2,930.6 3,564.9 3,564.7 3,564.7

---------------------------------------------------------------------------

Total Cash Operating Costs 1,763.9 1,990.5 1,829.0 1,829.0

---------------------------------------------------------------------------

EBITDA 1,166.7 1,574.4 1,735.7 1,735.7

---------------------------------------------------------------------------

Total Capital Expenditure 93.8 305.3 307.5 362.4

Initial 42.5 184.9 208.4 251.3

Contingency 2.9 27.5 30.8 39.5

Sustaining 60.5 105.0 80.3 83.7

Working Cap. Movement (12.0) (12.0) (12.0) (12.0)

---------------------------------------------------------------------------

Taxation Payable 361.2 431.5 485.7 467.1

---------------------------------------------------------------------------

Net Cash Flow after Tax 711.7 837.6 942.5 906.2

---------------------------------------------------------------------------

NPV 215.1 264.8 449.8 417.1

---------------------------------------------------------------------------

IRR N/A 34% 52% 41%

---------------------------------------------------------------------------

LOM (years) 27.0 21.0 12.0 12.0

---------------------------------------------------------------------------

Payback Period (years, undisc.) N/A 1.8 1.7 2.4

---------------------------------------------------------------------------

Payback period (years, disc at 8%) N/A 2.2 2.1 2.9

---------------------------------------------------------------------------

Operating Cost ($/t) 37.7 28.3 26.0 26.0

---------------------------------------------------------------------------

Operating Cost ($/oz) 388.5 360.2 331.0 331.0

---------------------------------------------------------------------------

Profitability Index 4.7 1.2 1.9 1.4

---------------------------------------------------------------------------

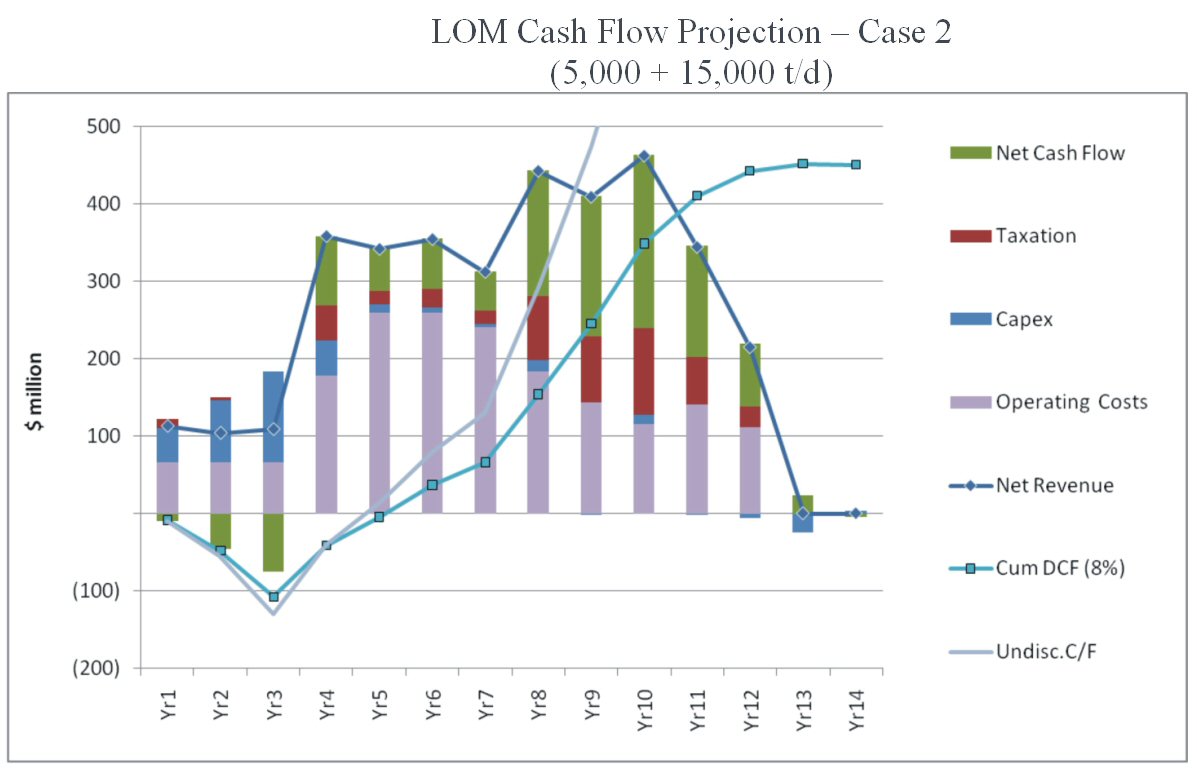

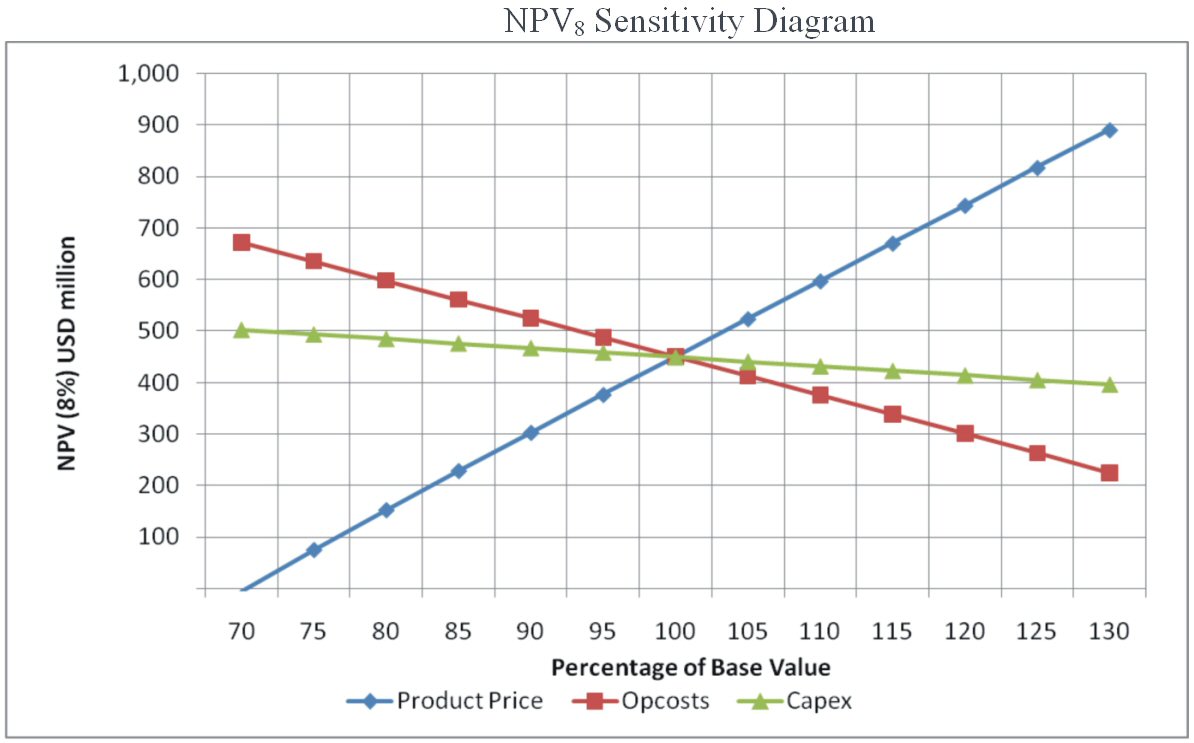

The following Figure shows the main elements of the LOM cash flow for the expansion to 20,000 t/d under Case 2. To view this Figure, please click on the following link: http://media3.marketwire.com/docs/rm... Study Sensitivity and Upside to Gold Price Above $US 700/oz The results of sensitivity analysis at a discount rate of 8% per year are summarized in the table below. Sensitivity to gold price is also presented in the following Figure, showing the NPV8 and IRR for Case 2 over a range of $US 250/oz above and below the base case forecast of $US 700/oz. Generally speaking, the project shows the most sensitivity to gold price, with lower sensitivities shown to operating costs and CAPEX. To view the Figure discussed in the above paragraph, please click on the following link: http://media3.marketwire.com/docs/rm... "Simply put, this is the reason why Rusoro purchased the Choco 10 mine; not for what it produces today - on average 120,000 oz/yr - but for what we think it can produce in the near future, over half a million ounces per year. The expansion project benefits from immense synergies resulting from the existing "brown-fields" infrastructure at the mine site, given that the Choco 10 mine itself has been in existence for over 4 years. This study further underscores our view of the immense value to be unlocked from our world-class gold deposits, Choco 10 and Increible 6", stated George Salamis, President, adding "We will continue to strive toward our goal of making Rusoro the next intermediate gold producer on an international scale". Andre Agapov, CEO of Rusoro, commented "There are surprisingly few gold projects remaining in the world today showing the qualities highlighted in the PEA: significant annual gold production, lower quartile on operating costs and a relatively long mine life. The production levels estimated in this study, would place the expanded Choco 10 - Increible 6 in a category within the top 25 gold producing mines, worldwide. Rusoro, being the only foreign mining Company who has thus far demonstrated an ability to produce gold in Venezuela, on a large scale, has the means and management to successfully develop such a mine on a grand scale." Future Studies and Development The Company is working to complete a Definitive Feasibility Study and the Environmental Impact Assessment by Q2, 2010. Additional infill drilling for the Choco 10 and Increible 6 gold deposits is scheduled to begin in the next few months. Updated measured and indicated resource estimates for both Choco 10 and Increible 6 are to be released before the end of Q4, 2009. Subsequently upon final pit design, mineral reserve estimates will be completed as part of a Definitive Feasibility Study. George Salamis, President stated: "We have an aggressive plan to move the Choco 10 expansion to production by the end of 2012. During the next nine months we will be focused on completing the Definitive Feasibility Study, optimizing the capital program and will be seeking the necessary permits for this four fold production expansion." Detailed Report Within the next 45 days, the entire Preliminary Assessment Study will be available at www.sedar.com and on the Company's corporate website at www.rusoro.com Note: This Preliminary Assessment Study is conceptual in nature as it is based partially on inferred resources at both Choco 10 and Increible 6, which at this stage do not have a high enough level of confidence to provide the economic basis for a production decision. The Company plans to complete its infill drilling program and additional study, which if positive, may advance the Project to the Definitive Feasibility level. Qualified Person The Preliminary Assessment Study was prepared by Micon International Limited. Qualified Person: Mr. Gregory Smith, P.Geo, the Vice-President Exploration of the Company, is the Qualified Person as defined by National Instrument 43-101, and is responsible for the accuracy of the technical information contained within this news release. About Rusoro Rusoro is a gold production, development and exploration company operating in Venezuela and is the only foreign gold miner in the country. The Company controls a large land position in the prolific Bolivar State region of Venezuela, operating on its own at the Choco 10 Mine and in a JV with the Venezuelan Government at the Isidora Mine. Ore from both mines is processed through the Choco 10 mill facility near the town of El Callao. The Company produced approximately 100,000 ounces of gold in 2008 and is working towards advancing two new gold mining operations in Venezuela. ON BEHALF OF Rusoro Mining Ltd. George Salamis, President |

{kind=link}

{kind=link}