II-VI: Growth Drivers By Competitors

posted on

May 26, 2017 07:35PM

https://seekingalpha.com/article/4076970-ii-vi-growth-drivers-competitors

II-VI offers similar growth compared to competitors and with less concentration risk.

Continues to be the most profitable in terms of margin.

One of the few players investing in 3D sensors.

What is Driving Overall Growth?

II-VI Incorporated (NASDAQ:IIVI) reported its FQ3'16 results despite concerns over slowing demand in China; revenue was $245 million, reflecting 22% YOY growth and 5.7% sequentially. Also, operating and net income showed an 11.8% and 8.5% margins, respectively, improving the middle and bottom line from the last quarter.

The main driver of the overall growth was its communications market with a 50% YOY growth, delivering $110 million in revenue, 82% of which was in Photonics. The catalysts that boost this growth were basically:

Breaking down revenue into product segments, it can be observed that Performance Products has not contributed much, remaining practically unchanged in the last five years. Given that this segment is military related and depends on defense spending and funding for U.S. programs, it seems that it will continue this way for the rest of the year as forecasted in the latest earnings call.

Source: Information extracted from 10-Q filing

On the other hand, Laser Solutions and Photonics are the ones that have contributed more on sales growth, especially the latter which has lifted revenues for the past five years. With an outlook for the next quarter of $245 million to $252 million in total revenues, the Photonics segment could grow roughly 28% annually in contrast with an apparent 9% growth coming from Laser Solutions.

Photonics is the most significant segment, which has improved considerably due to a communications market expansion and optical network upgrade. Its key products are passive components, assemblies and modules which are used for filtering, switching, combining and routing optical wavelengths within optical networks. There are also monitoring products that are used for measuring the performance of optical channels and systems. The Photonics products are mainly used to service the metro, regional and long-haul optical transmission markets.

There are other companies developing different technologies and services aimed at solving similar problems in the optical network market. The last annual report mentions a list of competitors by product segment, only a few appear in more than one, which make them more suitable for comparison. Lumentum Holdings (NASDAQ:LITE) and Finisar Corporation (NASDAQ:FNSR) compete in the laser solutions and photonics while Fabrinet (NYSE:FN) and Accelink Technologies Co. (SHE:002281) appear only in photonics but linked in more than one solution within this.

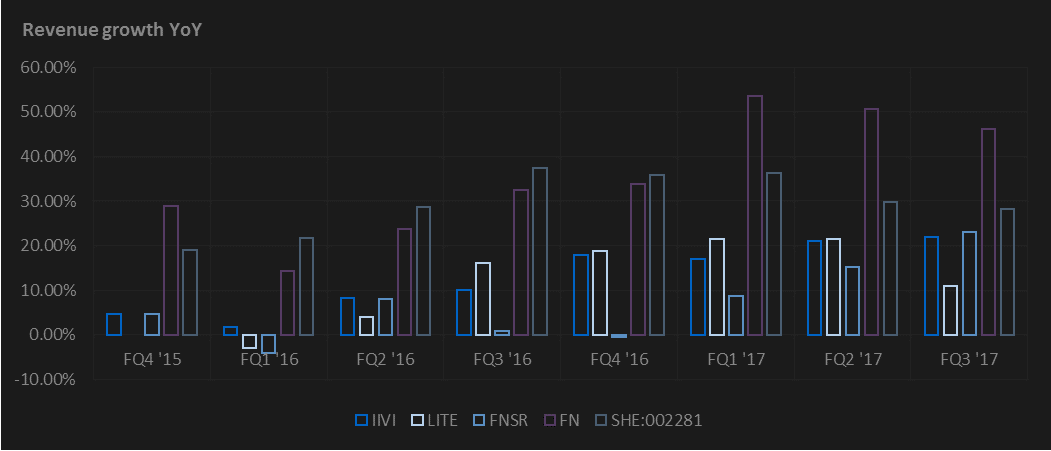

Growth Drivers by Competitors

Source: The data were compiled from several different sources from the SEC

The latest fiscal quarter, Lumentum reported $256 million in revenue, an 11% increase relative to a year ago and a 3.5% decrease sequentially. The main reason of this drop was due to softer demand from China and seasonal price reduction, mainly impacting the datacom segment which decreased 43% quarter on quarter. Its leading segment is also the optical communications, which continues to grow at 10% over the same period last year despite poor performance in datacom. The concentration in this segment is about 84% of total revenues or $216.1 million. Looking to the fourth quarter, the company has projected softer earnings, coming in the range of $220 million to $235 million on sales as a result of a decline in telecom from China.

In the case of Finisar, FQ3'17 revenues rose to $380 million, or 23% YOY, and a 2.9% growth compared to the previous quarter. Its key segment is also data communications applications that has contributed between 70% and 75% of revenue for the past five years. The lift in recent quarters was due to higher sales of its 100 gigabit transceivers, mainly from Chinese original equipment manufacturer customers, and also from sales of wavelength selective switches and ROADM line cards, although it expects a slowdown for the next quarter with revenues between $360 and $380 million, due mostly to seasonality and lower earnings from China.

Likewise, CASIX, Inc. (Private) appears as a photonics competitor in II-VI's annual report, with Fabrinet being the parent company. In the case of Fabrinet, revenue for the third quarter of 2017 came in at $367 million, a 46% increase YOY, supported heavily by its optical communications segment that can be split into datacom whose increase was 56% and telecom at 45% growth. The proportion of op-com segment is about 78% of total revenue. For guidance, revenue for FQ4 could come in the range of $361 million to $365 million or about 30% to 32% YOY due to a possible short pause in demand on its key customers.

Additionally, Accelink Technologies, a China-based company whose products are distributed primarily within the domestic market, is listed as II-VI's competitor within its optical amplifier modules. Given that Accelink's main source of revenue comes from the transmission products, which can provide optical transport network similar to II-VI, and it operates mostly in China, it has been added for comparison.

On its FQ1'17 report on April 27, Accelink had a 28% increase in revenues over the same period last year, coming at roughly $184 million. Its leading segments could be split into transmission products and access products with a 57% and 42% sales dependency, respectively. Similar to other players providing optical network products, the concentration of the top five customers represent 64% of sales. Also Accelink operates largely within China. For fiscal year ended December 31, about 80% of revenue came from the domestic market.

Given that the sales of II-VI are coming from different markets compared to its competitors, revenue growth has stayed at the same pace. Guidance is between $245 million to $252 million, expecting the next quarter to be equal or slightly better than the current while the others are forecasting a deceleration. Although it appears that other participants have benefited more than II-VI from the China broadband expansion, growth has been similar to its peers.

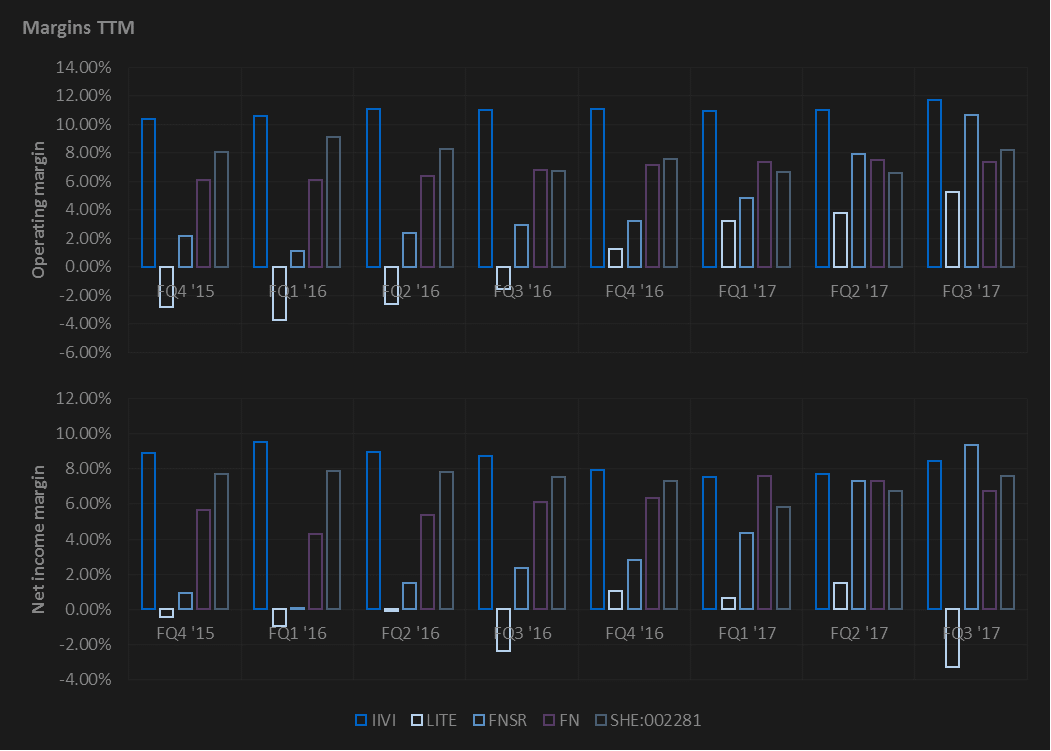

Profitability and Investment Overview

Source: The data were compiled from several different sources from the SEC

II-VI remains the most profitable within its competitors despite the cash outflow from this year's investment in the optoelectronic device platform. The operating margin for the current quarter was 11.8% compared to 9.5% from a year ago. Operating cash flow came in at $120 million on a TTM basis, remaining flat compared to the previous quarter. FCFE significantly decreased compared to prior results due to a rise in CapEx in all of its platforms, even though staying positive at $12 million. Additionally, executives are expecting to see results from the investments in 3D sensing coming by the next fiscal year, anticipating large volumes by the next calendar day.

On the other hand, the operating margin for Lumentum was 5.3% on a TTM basis. This improvement shows a better gross margin and higher volume from its most profitable products. Additionally, FCFE surges significantly to $410 million for the trailing 12-month period mainly due to a capital increase of $450 million through convertible notes with a seven-year maturity. This additional cash will be used for general corporate purposes, which may include capital expenditures, manufacturing capacity expansion, and working capital, as explained in the last earnings call. Also, these convertible notes could finance the company's manufacturing capacity for 3D sensors since analysts are projecting revenues from this segment starting from fiscal-year 2018 and significant growth coming by 2019.

In the same way, Finisar has seen an improvement in margins, mostly due to a favorable product mix and a reduction in general and administrative costs, finishing at a 10.7% operating margin on a TTM basis. FCFE soared to $674 million as a result of a CFO upturn from $194 million to $216 million and an issuance of $575 million in convertible notes due in December 2036. While the use of raising capital is not disclosed, it could finance an expansion of the laser factory in Allen, Texas, for 3D sensing products, which is expected to be completed in the second half of 2018.

Also, Fabrinet has slightly improved its operating margin due to leverage in operating expenses and growing revenue, coming at a TTM of 7.4%, even with a strengthening of the Thai baht and higher labor cost coming from it, as explained in the 10-Q. Likewise, CapEx continues to be in the same range at 4.8% of sales or an expense of $12.8 million for machinery and equipment and $1.6 million for acquisitions or intangible assets for the current quarter. FCFE improved from a loss of $4 million to a positive $25 million.

For Accelink, cash outflow came mainly due to an increase in labor services paid and a higher price in the purchase of goods, with an operating cash flow about $16.4 million and a similar capital expenditure of almost $10 million. The remaining FCFE stays at a loss of approximately $26 million. Its investments and expenditure on fixed assets continue to be similar to what is being observed in the previous quarter.

With all this in mind, the next growth driver seems to be in the 3D sensing market and its application for mobile devices, consumer electronics and automobile. II-VI, Lumentum, and Finisar are expecting to see a value increase by the next half of 2017 due to a new market opportunity beside their core business of the optical communications market. Note here.

Source: Compiled and calculated using information from the SEC

This revenue renovation could deliver significant growth to II-VI for the next years. The market has already discounted the growth coming from photonics at a premium compared to the five-year average ratios, and with few players currently investing in 3D sensing, the price could see a significant boost by FQ1 to FQ2 of 2018.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: All information for this article was derived from publicly available information. Investors are encouraged to conduct their own due diligence into these factors.This article represents the opinion of the author as of the date of this article. The information set forth in this article does not constitute a recommendation to buy or sell any security.