China's Gold Market Dominance (by Ben Kramer-Miller on SeekingAlpha)

posted on

Mar 10, 2015 10:31PM

Emerging Mid-Tier Gold Company - Timmins

A precursory glance at the gold market reveals a relatively bearish picture. The price is making lower highs and lower lows and appears to be on the path to break its $1,130/oz. low from late last year. Furthermore, the USD remains strong - supposedly bad for gold - and economic data in the U.S. appears to be relatively strong, which leads people to believe that the Fed will hike rates relatively soon. While I've argued elsewhere that the latter is bullish for gold perceptions trump reality in the near term, which is why sentiment is negative and the price fell sharply on Friday.

But while sentiment among U.S. gold investors has shifted from mild interest in 2011 to downright apathy today, we are seeing some incredible developments in the gold market that the mainstream financial press is not picking up. The Chinese have been working towards controlling the world's gold market, and they are about to be in a position to do so by becoming involved in the Gold Fix.

Let's take a step back and look at the Gold Fix, because this is something that isn't so familiar for people who don't follow the gold market closely. Twice a day, four banks (ScotiaMocatta, Societe Generale (OTCPK:SCGLY), HSBC (NYSE:HSBC), and Barclays (NYSE:BCS)) come up with a fix price for gold that is determined by buy and sell orders that they are seeing for both physical gold (e.g. bars) and paper gold (i.e. futures contracts and other derivatives). At 10:30 AM and 3:00 PM, the gold price is "fixed" and an announcement is made to this effect by the Chairman - Simon Weeks of ScotiaMocatta.

Purportedly, there are advantages to doing this, as outlined by the LBMA. I have reproduced them here:

While this is true, the fixers are incredibly influential because of the Fix price's visibility, and they can therefore influence how traders react in the market place. Furthermore, since the Fix price is determined by these banks' assessments of their buy and sell orders, those looking to influence the Fix can do so by placing a large order in one direction, or the other, around the time that the Fix price is determined.

Thus, it is no wonder that there are those who argue that large bullion banks such as those mentioned above are conspiring and colluding in order to use gold derivative contracts to manipulate the price, and analysis of gold's price action around the time of the day's fixes (especially the PM Fix) suggests that they wish to push prices downward.

That this is conspiratorial conjecture is utter nonsense. In fact, until recently, it was official central bank policy. During the 1960s, when the gold price was fixed at $35/oz., a consortium of central banks openly colluded to maintain this price despite the fact that the increase of supply of dollars during the 40s and 50s made that exchange rate unreasonable. The collusion effort is called the London Gold Pool. After the London Gold Pool manipulation effort fell apart, the State Department and Washington policy makers were quite open about their concern that the U.S. was losing most of its gold to foreign central banks and that the dollar hegemony outlined in the Bretton Woods Agreement would crumble.

As I outline here, Washington and the Fed organized an effort to demonetize gold in the 1970s, and while the gold price rose, they were successful in getting other central banks to stop accumulating gold. From that point on, visible efforts to control the price of gold have been nonexistent although there is strong circumstantial evidence that similar efforts have continued even to this day. This includes the rise of gold leasing and statements from central bankers that gold derivatives could be used to prevent the rise of the gold price.

The London Gold Fixing is a part of continuing efforts by bullion banks to control the price of gold. Evidence for this comes from Dimitri Speck, who is "The Gold Cartel" I reviewed on Seeking Alpha last year. Speck publishes statistical data that looks at the average intra-day price action in the gold market and finds clear anomalies right around the AM and PM gold fixes.

(click to enlarge)

This data is incredible. Since gold had risen from 1993 until 2012, the gold price has risen on an average given day by 0.03%. But just before the AM and especially the PM fixes, we see a sharp spike downward. In fact, the spike before the PM Fix is -0.03%. The PM Fix on average is the lowest price of the day to the minute. This runs counter to what one would expect - a slow steady increase throughout the day that is perhaps greater in the evening, given that there is a significant amount of Asian buying relative to Western buying. Since the above chart was compiled using nearly 2 decades' worth of data, the odds that this is simply a statistical anomaly are miniscule.

The Chinese have been accumulating gold for decades and it has reached a point where they are among the largest holders of gold in the world. Officially, the PBoC holds 1,054 tonnes of gold, which is a sizable amount for a country that held almost none until a few decades ago. But at the same time, it is not very much when we compare these holdings to official holdings of other nations.

[Source: Marcus Grubb (13 November, 2014). "Gold Demand Trends", "Latest World Official Gold Reserves", "Top 40 reported official gold holdings (as at January 2015)" is on the first page of the PDF file).

Many gold market experts believe that the Chinese have accumulated far more than this, and this is evidenced by the incredible net import numbers that we have seen in the past few years.

China has also become the world's largest gold producer, and none of this production leaves the country.

While it is impossible to know just how much gold the PBoC has accumulated, or even if it has accumulated anything beyond the 1,054 tonnes it owns, officially we do know that the Chinese are slowly working towards changing China's role in the gold market. We can see this in various efforts - many led by the Chinese - to decentralize the gold market by offering other exchanges and clearing houses that compete with the Western establishment of the COMEX, the LBMA, and the Gold Fix, which we have already seen is integral to Western banks' influence over the gold price. The clearest historical evidence of this is the Shanghai Gold Exchange.

The Shanghai Gold Exchange is a relatively new gold exchange that allows Chinese citizens and banks to buy and sell gold and related derivatives. While the exchange has been around since 2002, it has become more prominent since the financial crisis. In 2008, the SGE began to allow futures trading, and it requires banks to register with the SGE and to maintain minimum capital ratios in order to participate. In 2010, the SGE began offering ETFs as a way to satisfy growing demand from retail investors in China - Chinese demand for bars and jewelry has more than doubled since before the financial crisis.

Most recently, in September, the SGE set up 11 yuan-denominated gold contracts that need to be settled in physical gold. This is a significant development because in the West COMEX contracts are often settled in cash or simply closed out before the delivery date. COMEX trading volume in the futures market outweighs the amount of gold that actually changes hands by a large factor, and there is almost never enough gold available in COMEX warehouses for every contract to be settled, because sellers of contracts aren't necessarily required to put up physical gold as speculators. The SGE is therefore much closer to being a physical market that treats gold as a commodity rather than as just an asset to be traded, and this is a key selling point that will appeal to those looking for a simple way to buy and sell physical gold.

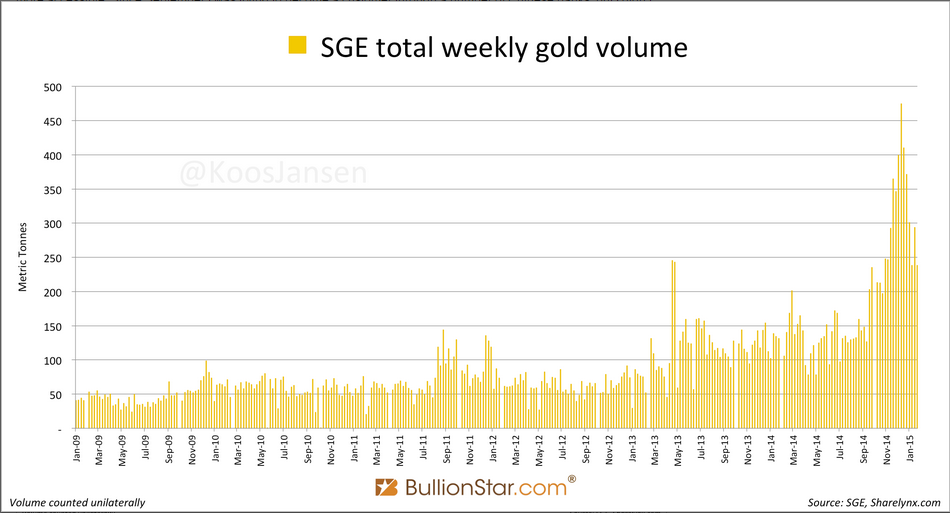

This is what Chinese banks and citizens are looking for. As the following chart illustrates, gold traded on the SGE has been on the rise.

(click to enlarge)

This volume is relatively low compared with the COMEX or even the Shanghai Futures Exchange, but COMEX trading is not rising. The three are compared on the following chart.

(click to enlarge)

At the bottom right of this chat, you can see where SGE volume picks up starting in September, and this reflects the aforementioned appeal of the physical market.

The fact that this has been going on demonstrates that Chinese officials and investors are unhappy with the current fixing system. They are slowly but surely moving away from this system.

Despite the rise of the SGE and its appeal as a physical gold exchange, the London Fix is still alive and well as a price setting mechanism controlled by the West. But this has the potential to change, and the Chinese are positioned to move one step closer towards becoming a powerful - if not the most powerful - player in the gold market.

The inspiration for me to discuss these topics was an article put out recently by Alasdair Macleod on goldmoney.com, in which he points out that the aforementioned London Fix banks will be handing over the Fix to the International Commodity Exchange. This will be a platform with greater regulation and oversight. But perhaps most importantly state-owned Chinese banks will be given a chance to participate, and this would break the cartel of HSBC, Barclays, ScotiaMocatta and Societe Generale. This is a big deal even if the Chinese banks don't come to "dominate" the process as Macleod indicates.

But while "dominate" is a strong word here given that China currently has no presence in the London Gold Fix, I do see why he is confident in his wording.

Macleod goes on to tell a very interesting story about China's long-term gold strategy, which he traces back to 1983. As a side note, Chinese officials have been masterful long-term thinkers in terms of their economy, and I've brought this up before in a discussion of their rare earth element policy (see part 3). Briefly, in that article, I point out how the Chinese came to dominate the rare earth industry from mining to ore processing to manufacturing over a multi-decade long period. Over this period, they developed an intellectual tradition that has given them a trade advantage that is arguably unparalleled by any other group in any other industry: They literally control more than 99% of the production of industrial-grade dysprosium and terbium, which are essential inputs into permanent magnets found in innumerable high-tech miniature gadgets such as smart phones.

China's gold strategy hasn't been in effect for as long as its rare earth strategy, but if you look at the select Articles that Macleod reprints in his article, it is clear that the Chinese want to restrict the amount of gold that leaves the country as a way for them to build up their gold reserves. Macleod points out that the 1983 goal was to ensure that the fruits of China's industrialization were preserved in an asset that doesn't have counterparty risk: gold. It has reached a point where it is the world's largest net importer and producer of the yellow metal. Nevertheless, the Chinese don't yet have the authority to participate in the most important gold pricing institution in the world.

China's participation has the potential to change that, because in a couple of weeks Chinese buy and sell orders will be able to influence the Fix price.

There are several different scenarios to consider and they are all interconnected. So there's no answer to this question from a near-term standpoint. But I want to at least lay out my thinking on the matter.

As Macleod suggests, since the Chinese have been accumulating gold, if they are in a position to influence the price higher, they will, because they want to be able to benefit as much as possible from this accumulation.

The notion that we will see higher prices is also supported by the fact that the SGE gold price typically trades at a small yet noteworthy premium to the COMEX price.

(click to enlarge)

On the other hand, if we assume that the upcoming Gold Fix changes are going to give the Chinese a greater say in prices, we should consider the possibility that this new power could be used to influence them lower as the Chinese accumulate more gold.

Ultimately, as Macleod says, this is extremely bullish for gold. Chinese banks will be in a position to impose their influence on prices, and since they have gold and are the largest player in the physical gold market, they will ultimately want prices higher. But will this happen on or just after the new regulations come into effect - March 20th - or will it take some time to develop? My near-term ambivalence leads to the conclusion that I simply don't know and that I want to avoid trading this market.

The Chinese are the largest players in the physical gold market, but they watch as European and North American bankers set the price based on a mostly paper gold market. The fact that the Chinese will soon have a seat at the table is one of the most important developments in the gold market in a long time.

We see that it is incredibly bullish, but not necessarily as a near-term catalyst. It is part of a long-term development whereby the Chinese have accumulated gold and influence in the gold market. So in that sense, March 20th will be a milestone in a string of many and I wouldn't necessarily trade it as if this isthe event whereby China's developing influence in the market will finally be made apparent to the world. The Chinese are secretive, and they are long-term thinkers, so I think that those who are expecting fireworks in a couple of weeks will probably be disappointed.

But the significance of the Chinese finally infiltrating the Western gold price fixing consortium should not be lost, and it confirms my thesis that despite the bearish price action, there are incredible bullish developments that make this one of the best markets to own long term.