Charts & Comments

posted on

Jul 22, 2011 02:29PM

Saskatchewan's SECRET Gold Mining Development.

Globe And Mail

The Globe weighs in on just why gold miners have underperformed so badly, laying the blame on the formation of ETFs.

John Ing maintains more bluntly that miners have surreptitiously gone to the market and paid for everything with shares.

I would put it more frankly, that gold miners are almost universally doted with freakishly bad managements. The sign of bad management is one that goes to the market dilutes the float with no consideration for the consequences. There probably isn't one stock out there in the gold mining sector that does not come with these warts and features. (there are some exceptions to the rule)

What investors are looking for are large, disseminated deposits which they can buy into very cheaply with no risk, with robust grades over large widths, who never intend in the least to pay out any sort of dividend to be bought out at a premium price by a mining major. Everyone wants the mania to be visited on them and their gold mining patrie, and if it hasn't happened, dilute to infinity to make up for the failures. Or, you have good prospects sold at a major discount, such as Brett Resources, Underworld, or Aurelian.

You might be lucky, and had an investment in Redback, which sold for 60P/E, and will cause headaches for Kinross for a long time to come. But where do you go when you want a dividend paying gold miner? There isn't a single one that lives up to their name's sake, being a company that mines gold and provides returns for the shareholders.

The failures are very apparent, but the gold has to be mined, refined and sold into market before it can be confiscated or swapped out. At least with an ETF, you have the sense that the gold in the vault is yours, even though it really isn't.

Financial Post

One mining company that has gone out of its way to absolutely destroy shareholder value is Lakeshore Gold. The dilution has been immense, all spent on upgrading the mill. You might have had an excellent mining company here, where the narrow vein grades were robust, but they opted instead for ignoring astringent grade controls.

There is no way they can ever fix the problem now. Huge dilution, emphasis on quantity of ore, rather than quality, and mining methods more suited to open pits in the rush to establish production numbers. And yet, nobody sees anything wrong with the results. Except, when it comes down to asking someone their opinion on how it measures up as an investment. On the dustheap it goes.

Golden Band has gone headlong down this route, their path to destruction. Will the same obsolete mining methods be employed in La Ronge and the investment go sour? (if it hasn't already)

Weekly Analogous Gold Chart

In the weekly gold chart, you can see the possibility of developing another major rounded top before a brief parabolic peak, as had occurred in 2005-2006. What the gold market is working on is a 40-year inflation adjusted average, which should now be in the vicinity of ~$2000/oz. U.S.

supersize: http://www.flickr.com/photos/11747277@N07/5964255889/sizes/l/in/photostream/

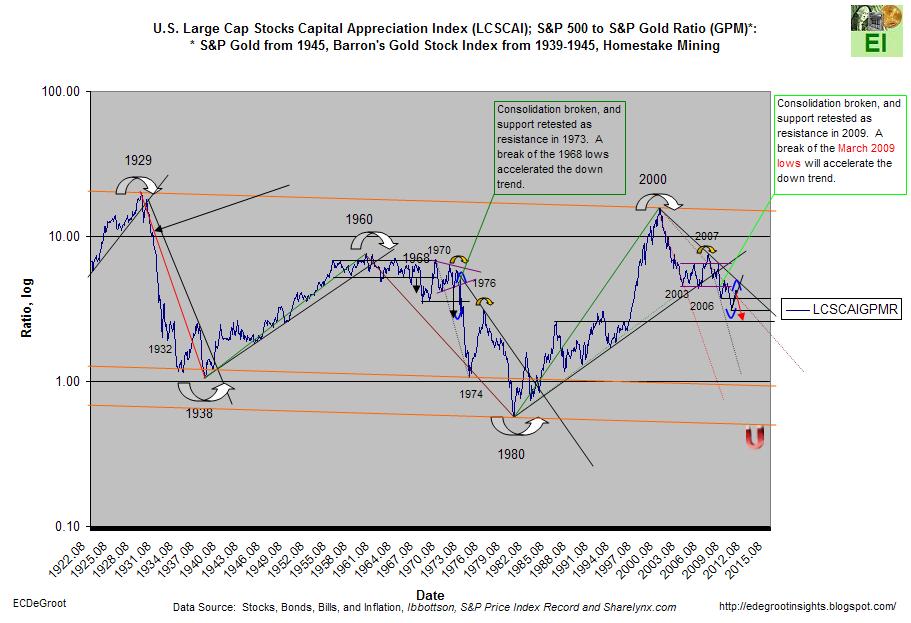

The loss of upward momentum in the stocks to gold stocks ratio suggests another down step

is coming. Gold stocks will outperform equities once the power up trend breaks.

U.S. Large Cap Stocks Capital Appreciation Index (LCSCAI); S&P 500 to S&P

Gold Ratio (GPM)*:

* S&P Gold from 1945, Barron's Gold Stock Index from 1939-1945, Homestake Mining

source: http://edegrootinsights.blogspot.com/2011/07/controlled-steps.html

-F6