Should You Pay Up For This High Growth, Low Cost Silver Producer?

posted on

Jul 10, 2013 11:47AM

ONE COUNTRY, ONE METAL

Disclosure: I am long AG. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This article is about First Majestic Silver (AG), a highly profitable silver mining company with five producing mines in Mexico.

1: About First Majestic Silver

First Majestic Silver currently has a market capitalization of around $1.25 billion. It anticipates that it will produce 11 million ounces of silver this year, and this should increase by 50% over the next three years.

First Majestic is among the most expensive silver miners based on several key metrics (price/annual production, price/silver reserves, price/tangible book value...etc.), yet there is good reason for this. First Majestic is one of the best managed mining companies of any in the world. It has demonstrated consistent production growth, and it achieves this growth through a highly disciplined strategy. The company only purchases mines that meet the following criteria:

While the company does not execute this strategy flawlessly, it has done a phenomenal job of mostly sticking to it. Of the six mines the company has in production, or intends to have in production over the next couple of years, only La Guitarra is not profitable at the current silver price, and only Del Toro has significant exposure to metals other than silver.

For investors who are looking for a company with exposure to the price of silver without any of the additional risk baggage that comes with so many companies, this is the company to buy.

2: Resources and Production

A: Resources

First Majestic Silver has five producing properties, another that will begin production in 2015, and some smaller exploration properties that it acquired after purchasing Silvermex Resources (which it purchased primarily for its La Guitarra property).

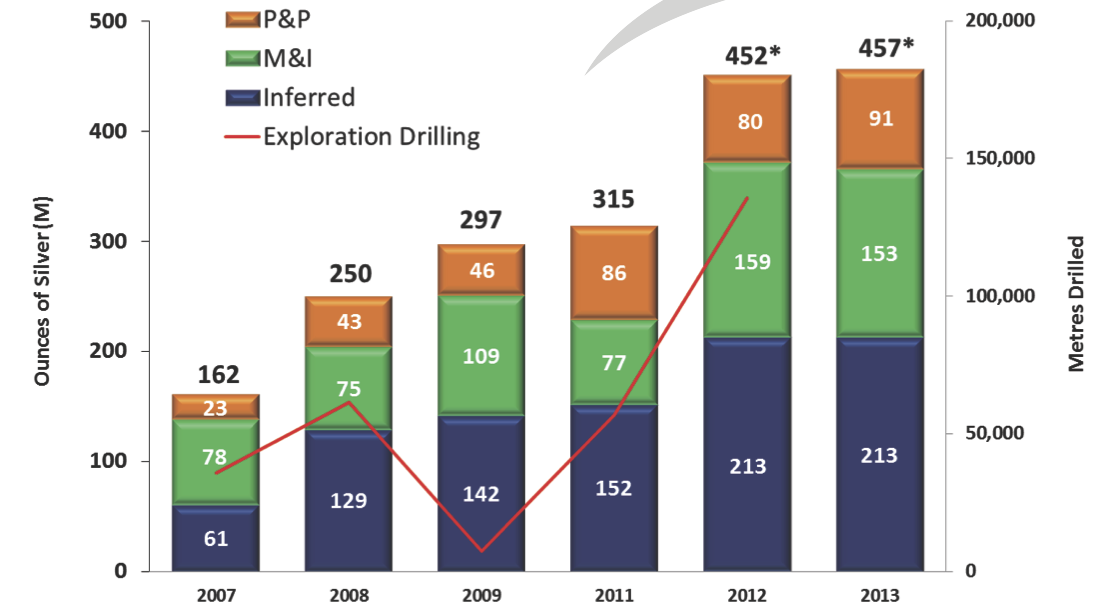

In all the company has an estimated 457 million ounces of silver as follows (in descending level of certainty/accuracy):

B: Production

All of First Majestic's silver is relatively high grade, with its properties typically having resource estimates between 100 grams per ton and 200 grams per ton. As a result all of its properties, except La Guitarra, are expected to be profitable even at today's silver price. I will discuss these properties in greater detail below.

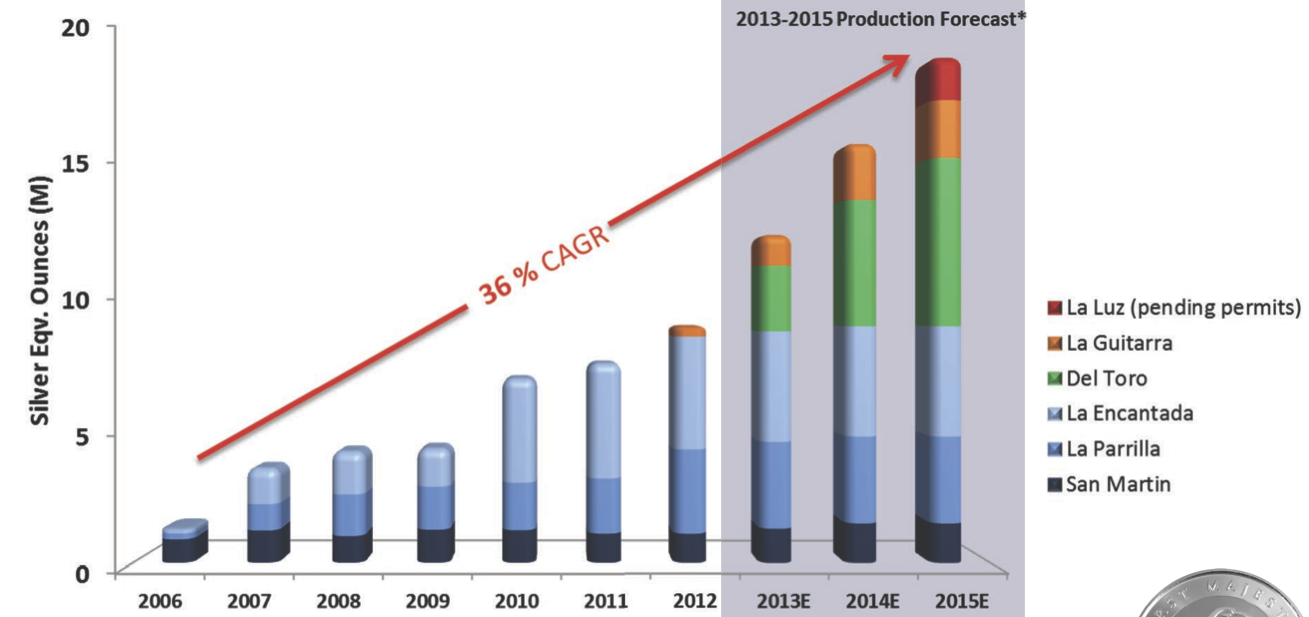

In addition to the company's high grades and low production costs, it has consistently grown its production: it has done so at an annualized rate of 36% according to its own figures. The following chart illustrates this

Given the company's low production costs and growth in annual production, it has enormous potential to grow its cash flow over the coming years. The following chart conservatively estimates this cash flow for 2013-2014 at various silver prices assuming $16/ounce "all-in" costs (which includes exploration, repairs, administration...etc.), 11 million ounces of production in 2013, and 14 million ounces in 2014.

| Silver Price | 2013 | 2014 |

| $15/ounce | -$11 million | -$14 million |

| $20/ounce | $44 million | $56 million |

| $25/ounce | $99 million | $126 million |

| $30/ounce | $154 million | $196 million |

| $40/ounce | $264 million | $336 million |

| $50/ounce | $374 million | $476 million |

| $100/ounce | $924 million | $1,176 million |

While First Majestic will lose money if the silver price continues to fall, its shares offer enormous leverage to the upside should the silver price resume its long term uptrend.

3: First Majestic Silver's Properties

All of First Majestic Silver's properties are located in Mexico. Currently, the company has five producing silver mines and one in development that should begin production in 2015.

In what follows I provide a brief description of each property.

A: La Guitarra

La Guitarra was acquired by First Majestic Silver when it purchased Silvermex Resources in 2012. The company is reticent to release information regarding the mine's reserves and resources as it reviews the NI 43-101 (a technical geological report used by mining companies) that was released by Silvermex. However, we can estimate this data from numbers released by Silvermex: 11 million tons at 113 grams of silver per ton, and 0.93 grams of gold per ton in reserves, which equates to:

*I must stress that First Majestic Silver does not endorse these numbers!

First Majestic has been ramping up production from 350 tons of ore per day to 500 tons per day, and the company anticipates that the mine will produce 1 million ounces of silver in 2013 and 2 million ounces in 2014 and 2015.

La Guitarra is by far the highest cost mine in First Majestic's arsenal, with estimated costs at nearly $16/ounce, but this number jumps $6/ounce to $22 if we consider the company's all in costs (including exploration, administration...etc.). Thus at the current silver price La Guitarra is losing money, although it is the only First Majestic mine that is in the red. Investors should also keep in mind that as the mine produces more silver it will likely become more efficient and costs will come down.

B: Del Toro

Del Toro began production earlier this year, and it is projected to be the company's largest producing mine. This mine more than any other belonging to First Majestic has significant exposure to metals that aren't silver (mainly zinc and lead). Currently the company estimates that the property has about 90 million ounces of measured and indicated silver, and about 160 million ounces of measured and indicated silver-equivalent ounces (zinc and lead expressed in terms of silver). The following table breaks this information down.

(click to enlarge)

The company expects to produce 2 million ounces of silver in 2013, and this number should improve to 4 million ounces by 2015 as the company increases the amount of ore mined from 1,000 tons per day to 4,000 tons per day.

Del Toro has incredibly low production costs of just $7/ounce, or $13 per "all-in" ounce. Thus Del Toro can withstand continued weakness in the silver market while at the same time it can offer investors significant leverage to the silver price.

C: San Martin

San Martin has been a stable producer for decades, although it was acquired by First Majestic in 2006. The property has almost exclusively silver resources which is why the property was so appealing to First Majestic. The company estimates that the property has 22 million ounces of reserves and 62 million ounces of resources, although most of the latter are "inferred," which is the lowest level of certainty in mining jargon. The following chart breaks down the property's resources.

(click to enlarge)

The mine has been a stable producer of roughly 1.1 million ounces of silver annually during the time frame that First Majestic has owned it, however the company points out that San Martin has never been explored using modern techniques and technologies, and it anticipates that it will find additional resources and be able to increase production over the next few years.

San Martin has cash costs of just under $12/ounce, or $18 "all in" so the mine is slightly profitable at the current silver price of just under $20, and it should offer significant leverage to the silver price to investors.

D: La Parrilla

La Parrilla is First Majestic's largest property in land terms. It has been in production since 2004, and has shown meaningful expansion in terms of both resources and production.

Currently the company estimates that the property has just over 30 million ounces of silver reserves and nearly 18 million ounces of silver resources. If we include the property's lead and zinc to calculate silver equivalent figures the estimates jump to 39 million ounces and 23 million ounces for reserves and resources respectively.

(click to enlarge)

Parrilla is currently one of First Majestic's largest producing properties at an estimated 3.3-3.4 million ounces of silver in 2013. The company has done an excellent job in ramping up production here from just 180 tons of ore per day when production commenced to 2,000 tons today, and this figure is up from the recent figure of 850 tons.

Parrilla is one of First Majestic's most efficient projects with all-in costs of $14.40/ounce, which means that the mine is highly profitable even at the current silver price.

E: La Encantada

La Encantada is currently First Majestic's largest producing mine, although Del Toro will take over in the coming years. It is also the company's "purest" silver mine with nearly all of the resources being silver.

Currently, the company estimates that the property has 39 million ounces of reserves at 156 grams per ton and 34.5 million ounces of resources at 181 grams per ton.

(click to enlarge)

The company estimates that the mine can produce 4.2-4.5 million ounces of silver at full capacity, although it unfortunately will not be growing production at La Encantada. Furthermore, given the size of the property's resources this is not a long-life mine, and I suspect production will begin to decline over time. However, it will provide significant cash flow for the company over the next few years, and the company can use it to acquire other properties that will have significant production in the future.

Currently, the company estimates that costs at La Encantada are just under $8.50, or approximately $14.50 "all-in" meaning that the mine is very profitable at the current silver price, and it can withstand a further silver price decline while still offering significant leverage to the price of silver.

F: La Luz

Of the six properties that are or will be in production La Luz is the smallest in terms of resources, with just under 47 million ounces (I exclude La Guitarra). However the silver at La Luz is very high grade, averaging over 200 grams of silver per ton.

La Luz is slated to be in production starting in 2015. The company anticipates being able to produce around 1.5 million ounces annually. It has not yet released production cost estimates, although given the high grade of silver at La Luz I suspect that the cost will be relatively low.

G: Exploration

First Majestic Silver is not really in the business of exploring properties that do not already have extensive resources: it strives to find late stage projects in order to develop and expand them. When it acquired Silvermex Resources, in addition to getting Guitarra the company also received several exploration properties, including the four I mention below.

4: Risks

A: The Price of Silver

The price of silver has performed terribly over the past two years, having declined from $48/ounce to under $20/ounce. While there is significant technical support at the current price the downtrend that began in May, 2011 is still intact.

Most silver producers cannot turn a profit at the current price, and this is both a reason that the silver price has likely reached or is near to a bottom, and a reason to like First Majestic Silver as a company that is a low cost producer. Still the downtrend in the price of silver is intact, and the company's profits will be closely linked to the price of silver.

B: Valuation

From the cash flow data I present above, it appears that First Majestic Silver is overvalued: for instance, with a market capitalization of roughly $1.25 billion and a silver price of $20/ounce, the company trades at 26-times 2013 cash flow. However compared to the company's historical 36% CAGR in production the price seems reasonable.

In order to justify paying this price for First Majestic shares, investors have to be convinced that the company will be able to execute as it has in the past. Yet as the company grows it will become more difficult to find projects that fit its unique profile of high grade silver mines that are located in Mexico with limited exposure to other metals. Ultimately I do not think that the company will be able to maintain its 36% production growth rate without loosening its standards for choosing mines.

That being said I would want to wait for a better entry point relative to its estimated cash flow. Rather than paying 26-times estimated cash flow I would feel much more comfortable paying 15-times. This is more than I would pay for other mining companies given the volatility of metal prices and the fact that mining is a difficult business, but the fact remains that First Majestic is probably overvalued: if 15-times cash flow is a fair valuation and a $20/ounce silver price is assumed, then the shares are worth a mere 57% of what they are currently trading at. If, however, we assume that silver trades at $25/ounce, then at 15-times cash flow and $108 in 2013 estimated cash flow, the stock is worth $1.62 billion, which would give the stock 30% upside.

Conclusion

First Majestic Silver is one of the best silver producers for investors who want exposure to the silver price without the risk that the company falters while the silver price languishes. It is one of a few silver mining companies that is profitable at the current silver price of around $19/ounce. Furthermore, it is growing production regularly and it has proven itself able to execute a disciplined plan geared towards value creation.

That being said there are reasons to look elsewhere. First, the company's shares are probably over-valued. Second, for investors who want explosive leverage to the silver price, this is probably not the best stock to own. Investors who believe that the price of silver will increase dramatically (to, say, at least $100/ounce) should look at producers that require higher prices to be consistently profitable, or to bring new mines into production (e.g. Silver Standard Resources, or Arian Silver for high rollers).