ANALYST VIEW - UBS upgrades Hungary's MOL to 'Buy', raises TP

posted on

Jun 02, 2010 09:09AM

Developing large acreage positions of unconventional and conventional oil and gas resources

|

June 2, 2010, 9:51 am

|

http://portfolio.hu/en/cikkek.tdp?k=1&i=20216

UBS has on Wednesday upgraded Hungarian fuels group MOL to 'Buy’ from 'Neutral’ and raised its target price for the stock to HUF 22,000 from HUF 21,500, citing an updated by the company on its Kurdistan project as the main reason. UBS said MOL is its preferred stock in Central and Eastern Europe, with several catalysts absent elsewhere in the CEE peer group that could drive the share price.

MOL and its Croatian subsdiary INA held an Investor Day in Pula (Croatia) last week, focusing the presentation on the E&P and R&M businesses.

"In E&P, the strategy for the domestic onshore assets is to try to stem the decline, while growth (both reserves and production) will mainly come from its international upstream portfolio, in particular Kurdistan, Pakistan, Syria and Kazakhstan," UBS cited MOL as saying.

"We believe the current share price offers investors an attractive entry point into a stock, which is expected to have numerous catalysts in the second half of this year, in particular from Kurdistan," UBS said in a research note published today.

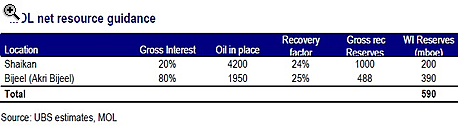

Much of the reserve upside that MOL is targeting over the next three years comes from its international E&P portfolio, with at least a third from Kurdistan, UBS noted.

"MOL was very upbeat on the prospectivity of its Kurdistan assets, Shaikan and Akri Bijeel. Its pre-drill estimate of net recoverable resources of 590mboe only includes one prospect on Akri Bijeel and does not include the potential upside from Shaikan also. The Bijeel-1 is indicated to exceed pre-drill estimates, and the discovery has also de-risked the other prospects it will target over the next 12 months."

In R&M, UBS sees "very little progress" on the Phase II refinery upgrade plans of the Sisak and Rijeka refineries. In particular related to the Rijeka refinery, where in Phase II MOL intends to add a residue upgrading unit, MOL has yet to receive government approval, it noted.

"Should MOL not receive government approval for the Rijeka upgrade by year end, we see downside risks to our EPS estimates," UBS added. The investment bank’s EPS estimates are HUF 1,602. for 2010, HUF 2,046 for 2011 and HUF 2,381.5 for 2012.

The HUF 22,000 TP is set at a 10% discount to UBS’s SOP valuation.