GOING FOR GOLD

posted on

Apr 15, 2008 02:21PM

The company whose shareholders were better than its management

Beating inflation is what investing in the stock market is all about. Risk-averse investors can’t rely only on nominal returns because they don’t necessarily exceed inflation. If you are an investor that can take risks, your primary measure of success is how well you did against an index. Of course, there are indices for almost everything, so let’s use the S&P 500, the measure many of our readers would love to beat.

Alpha is any gain above the return of the S&P 500. If you’re picking stocks or paying someone to do so, it can be very costly if you do not beat the underlying index of stocks.

This article illustrates the fact that beating the S&P 500 since the “dot com” bubble should have been a no-brainer, and why this could continue to be possible in the next few years.

In August, when the market finally reacted to the liquidity crisis, the Federal Reserve had a few choices. These included lowering interest rates and increasing the money supply, doing nothing, or even raising interest rates and letting the market purge some of the “mal-investments” of the last few years. The choice made was predictable: lower interest rates and inject liquidity into the system. By definition, this has increased the money supply, which is equivalent to creating inflation: the policy has caused more dollars to “chase” the same number of goods.

Wall Street cheered this decision. But the actions of the Fed have not helped individuals who own dollar-denominated assets in stocks, bonds or cash. The indices have since bounced off their August lows, but the credit crisis has not been fixed. The more the Fed increases the money supply, the worse the situation becomes, and the longer it takes for the situation to correct itself. Meanwhile, the value of the U.S. dollar has dropped to an all time record low since the dollar was officially removed from the backing of gold in 1971.

This is a big deal: when the US dollar loses value, the cost of products goes up. So it’s not how many dollars you have, it’s what they will purchase. There are serious risks to holding all your investments in dollars.

When the average investor discusses stocks and bonds, it’s to be expected that stocks have higher rates of return because they also have higher risk. A basic comparison would be the S&P 500 vs. the 10 year Treasury bond. Let’s also add the relative value of the dollar against other currencies and money with actual intrinsic value. Gold exemplifies a material used as money because of its intrinsic value.

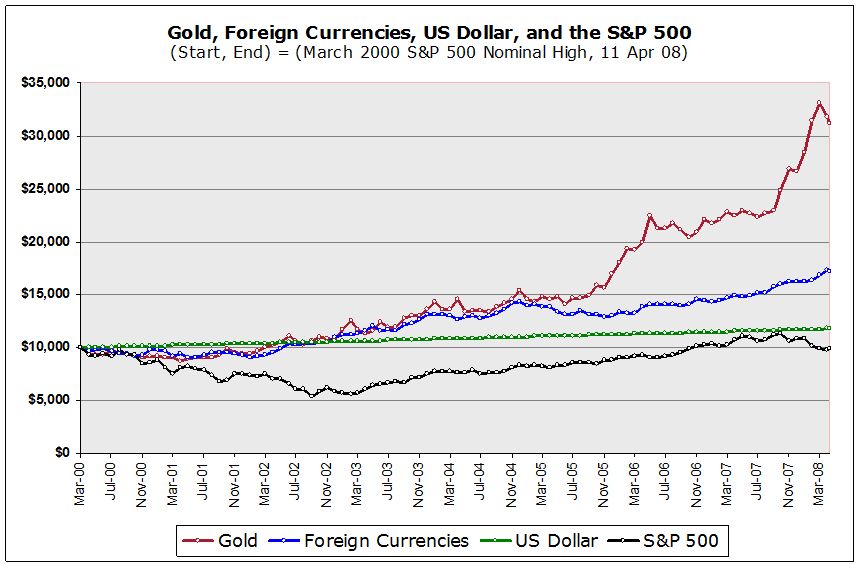

The chart below takes a look at the returns of a $10,000 investment in the S&P 500 starting from two points: the March 2000 high during the “dot-com” peak, and the September 2002 lows when the index began to recover. Also shown are returns of a $10,000 investment in the 10 year bond, foreign currencies through the Dollar Index, and gold bullion. Clearly, US stocks as defined by the S&P 500 have underperformed, thus the bear market.

The Dollar Index measures the value of the Dollar vs. a basket of currencies that include the European Euro, Japanese Yen, British Pound, Canadian Dollar, Swedish Krona, and Swiss Franc. Gold is used as a comparison because, other than silver, it’s the only form of money that has intrinsic value, whereas fiat currencies are merely paper whose value is based on confidence. In fact, gold has been used as money since it was discovered. And depending on various estimates, the annual global supply of gold only increases anywhere from 1 to 2.5 percent.

click to enlarge images

March 2002 Starting Point:

If you chose to invest in the S&P 500, you would have had a real disaster. Of course, if you had chosen to begin investing in the S&P 500 at the start of this timeframe, your disaster would have been created in part by the worst possible timing. Regardless, note how badly the Dollar did against foreign currencies and gold.

Summary of Returns since March 2000:

The Dollar has, at best, returned the rate of inflation. Foreign currencies out-performed and gold has provided the best return. The fact that gold has out-performed is not an accident; remember, paper money can be printed at much faster rates than gold can be produced. And with the Federal Reserve increasing money supply at faster rates than foreign central banks, of course the U. S. dollar has under-performed.

Since the height of the “dot-com” bubble, the worst store of value has been the S&P 500, followed by US Dollars.

September 2002 Starting Point:

Here again the Dollar loses big to foreign currencies and gold. The S&P 500 did well, but gold still out-performed. Is it coincidence that gold began to decisively out-perform starting at the peak of the housing bubble?

Summary of Returns since September 2002:

Even though the starting point of the S&P 500 is its “post-dot-com” bottom, gold still out-performed. And foreign currencies did even better against the Dollar. At some point, the Dollar will bottom, but until money supply ceases to grow at double digit rates, the Dollar will likely be under pressure.

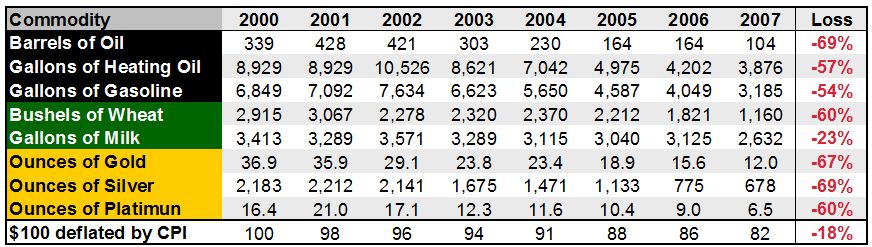

Remember, gold doesn’t pay interest, and it still beat the Dollar and foreign currencies. During the period we have examined, holding US dollars has resulted in a loss of purchasing power. Here’s a look at how holding Dollars has reduced purchasing power from 2000 to 2007.

How much US$10,000 purchases:

This data, along with housing costs over the last seven years essentially means the CPI is “official” inflation, while consumers pay “real” inflation. Regardless, the loss in purchasing power is no accident; there are many reasons why the Dollar has performed so poorly.

There are many reasons why the dollar has lost value. Key reasons include:

Inflation has been rampant. To be sure, inflation is defined as an increase in the supply of money and credit. The Federal Reserve has been creating so much inflation that prices naturally go up to make up for the extra money and credit chasing the same amount of goods. A check of John William’s Shadow Stats show how the M3 money supply has been growing at double-digit rates!

While the consumer price index seems to show that inflation is not a problem, this index does not reflect food and energy costs to households. As a result, at the moment the investment community may have underestimated the true US inflation rate.

Interest rates are low compared to other currencies. While US interest rates are some of the lowest in the world, they are even lower when adjusted for inflation. In fact, if it wasn’t for the government’s method of calculating inflation, real interest rates on Treasuries would have been negative in the last few years.

Consumers are running out of steam. This has been argued many times and the consumer seems to always come through. But let’s look at the fundamentals. We know that housing is in a recession; this has effectively eliminated the use of home equity as an “ATM machine” for most US households. The retailing and domestic automobile industries are experiencing a recession. Meanwhile, the recent small rise in exports has not offset the trade deficit.

Trade deficits have continued. Each year the US has to create more dollars to pay for our consumption. Even with the already weaker dollar, US exports have not increased enough to balance the trade deficit. In fact, one could argue that a weaker dollar puts pressure on U. S. manufacturers through higher commodity prices.

Budget deficits have continued. The US government continues to borrow and spend, increasing the national debt. Some would argue that debt as a percentage of GDP is actually under control, however, just like we’re seeing entities tied to the US housing market take major hits due to declining asset values, there is a similar risk in that debt as a percentage of GDP can increase dramatically if GDP contracts.

So, how will the Dollar perform over the next few years? As some of you may have seen, Jay-Z’s new video flashes crisp new 500 Euros bills. But how much longer will the world loan the US money so that Americans can enjoy goods produced by foreigners in exchange for IOUs? It is likely that they will continue their willingness to loan the US money, but perhaps at increasing rates of interest. In the longer term, perhaps they will insist on loaning the US money in their own currencies, not in US dollars.

The key reasons for a continued decline include:

The Fed and foreign central banks will create even more inflation. Keep in mind that many US Dollars are held by foreign central banks and not foreign individuals. Foreign central banks fully intend to convert many of these dollars into US assets. We have already seen the creation of Sovereign Weath Funds by the likes of China, Singapore, and Abu Dhabi. When SWF’s purchase US assets, they must first sell their treasuries in the open market in order to convert to cash. As the pattern of selling continues, more downward pressure on the dollar is applied.

Interest rates could rise. As the world sees that the US cannot pay back existing loans, they will demand higher interest rates to provide Americans with credit. Depending on the extent to which foreigners lose confidence in the Dollar, they may begin to stop loaning us money in US Dollars, choosing instead to loan Americans money in their own currencies in order to avoid US inflation. This will have a profound effect on our economy because the cost of capital will go up.

The Dollar is officially trading at artificially high rates. There are many countries who still peg their currencies to the US dollar, some for good reason, but in others, the peg is causing inflation. Pegs include Saudi Arabia, U.A.E., Hong Kong, Venezuela, and Costa Rica, among other smaller nations. Look for many of these pegs to either change to a basket of currencies (including the Euro) or dropped altogether.

When the Fed recently reduced the Fed funds rate, the Saudi Arabian government refused to reduce their interest rate to match ours. If the unofficial (real) Saudi riyal to US dollar exchange rate begins to materially differ from officially rates, a black market could develop.

The trend here is simple, the US dollar is continuing to lose value relative to other currencies and commodities. In order to defend from the worsening fundamentals, investors should diversify away from US dollar denominated assets.

For purchasing power preservation:

For more aggressive investors:

Visit the Portfolio Allocation section for more details on portfolio investment strategies.

Don’s January Investment Ideas

Gold has traditionally been a small percentage of an investors portfolio, so for all the reasons above, invest in gold bullion, our official pick. For those interested in additional leverage, a Gamco Gold mutual fund.