EQUEDIA WEEKLY REPORT ******

posted on

Nov 04, 2012 06:41PM

We may not make much money, but we sure have a lot of fun!

Dear Readers,

Are we finally about to crash and burn?

Friday's entire stock market action was disappointing, despite a series of positive economic data which, as we all expected, came out extremely positive days ahead of the election.

According to the last job market report, payrolls in October expanded by 171,000 workers; far exceeding expectations of 125,000.

Did the overly positive numbers surprise me? Not one bit.

In the weeks prior (see Another Record High and A Global Gold Controversy), I talked about how these numbers are calculated and manipulated to induce euphoria into voters before the elections.

However, even with the strong numbers, the market stalled Friday with Apple continuing to hurt the market. I think the market is starting to understand; the numbers show us nothing. Does that mean the good news is now fully priced in? If that's the case, where is the market headed?

A Storm is Gathering

Next week's U.S. election will be at the forefront of market activity. But there are some other critical things we have to watch out for in the coming weeks: the Fiscal Cliff and debt ceiling debate, another Spain bailout, and the further collapse of Greece.

That's right, Greece risk is back.

Greece Risk is Back

Two weeks ago, Greek Prime Minister Antonis Samaras said Greece would run out of cash on November 16 and said it is crucial that a decision on sending further aid to Greece is made at the upcoming meeting of eurozone finance ministers on November 12.

But before aid will be considered, Greece will be forced to vote on controversial labor reforms demanded by the Greece's troika lenders (EU, IMF, ECB), which some factions of parliament are strictly opposed.

While Greece's finance minister Yannis Stouranaras tried his best to reassure us that he was "fairly confident" that the vote would pass, the governing coalition is still facing dissent in the ranks.

Bank of America's rates strategist Max Leung writes:

Next week, the Parliament will vote on the austerity and structural reform package for the first review of the new program. The risk of a negative vote is real, as both PASOK and the Democratic Left, the second and the third parties in the coalition respectively, are threatening to vote against the package. In addition, the Greek debt sustainability and the financing of the €20-30bn shortfall in the EU/IMF program are issues yet-to-be resolved.

Deutsche Bank strategist Jim Reid highlights in his latest note a whole other complication introduced to the Greek situation last week:

Back in Europe, the main headline was that the Greek Court of Auditors sees the pension reforms demanded by the troika as unconstitutional, potentially derailing the government's efforts to push through its EU13.5bn austerity package through parliament next week...broader equity markets shrugged off the headline, but the Athens Composite equity index closed down 5% on the day, and is now down 13% on the week.

According to Societe Generale strategist Vincent Chaigneau:

The new budget numbers unveiled on Wednesday are somewhat astonishing. The Debt/GDP ratio is now seen peaking at 192% in 2014. Compare this to the IMF's previous worst-case scenario that had a peak at 171%. The IMF won't pay its share of the next tranche unless it can be reassured that the debt can return to a sustainable path. While the IMF may be convinced that Greece needs to be given two more years (2022) to reach the 120% target, even that will be a challenge.

The IMF supports OSI, i.e. haircuts on official creditors (but not the IMF itself). Yet European governments look very much opposed to forgiving debt. The Greek parliament has just approved (narrowly) a law that will give the government flexibility to privatize public utilities. Speeding up privatisations will help, but that won't be enough.

Buybacks of the PSI bonds (€63bn outstanding), along with interest rate reduction and maturity extension on official loans, currently seem the preferred route for reducing the debt load. But who will fund those buybacks? Most likely that will imply new official loans, which will make the exposure of the official sector to Greek credit risk ever bigger.

In other words, more money will be printed to prolong the inevitable demise of Greece.

By 2016, Greece's debt would rise to 220.4 percent of GDP in 2016. In raw figures, the numbers are massive. The debt had already shot up to 329.5 billion euros in 2010 and forecasted to reach 411.9 billion euros in 2016.

As Pimco's managing director Andrew Bosomworth said:

"It's extremely difficult to see any way, any possibility how the country pays back its debt without receiving assistance in the form of debt relief...Greece is insolvent and it's going to default. It's just a question of how and when that is realized."

Spain - Another Bailout?

Spain is still a mess and they're under the impression another bailout isn't needed. We'll see what they say after their big bond auction next week. I see more risk on the table.

Nearing the Fiscal Cliff and Debt Ceiling

A month ago, the US closed the book on Fiscal 2012 with more than $16 trillion in debt.

The current debt is now at 16.229 trillion, and the ceiling at $16.394 trillion. That means the US has $165 billion in incremental debt capacity left before it breaches the federal debt limit.

U.S. Treasury officials expect the government will hit the current debt borrowing limit by the end of this year. But they said they can employ "extraordinary" measures that have been used in the past to keep the government functioning until Congress votes to increase the debt ceiling early next year.

Straying so close to the debt limit - not to mention hitting it - probably would lead to a second downgrade of the U.S. credit rating; proven already on January 30, 2012 when the limit was raised to a new high of $16.39 from $15.194 trillion set on September 2011.

There is no way that the U.S. will be allowed to default. Both Republicans and Democrats know that.

So it's not a matter of will they raise the debt ceiling; it's a matter of what it comes with. For example, the opposing party might only vote on the debt ceiling if it is accompanied by major spending cuts and long-term debt reduction; something we witnessed in the last debt-ceiling debate.

Because the U.S. will soon breach its debt ceiling, it will add even more urgency to efforts to avoid the upcoming fiscal cliff.

The United States fiscal cliff refers to a large predicted reduction in the budget deficit and a corresponding projected slowdown of the economy if specific laws are allowed to automatically expire or go into effect at the beginning of 2013. These laws include tax increases due to the expiration of the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 and the spending reductions ("sequestrations") under the Budget Control Act of 2011.

If the fiscal cliff is not avoided, the adverse effects on the economy could push the country back into recession; thus wiping out all of the efforts accomplished (if any) since 2008 and wasting trillions upon trillions of dollars.

Meanwhile the U.S. government continues to run record deficits. For the 2012 budget year, the deficit totaled $1.09 trillion, the fourth consecutive year that the deficit has been over $1 trillion.

As we near the debt ceiling and fiscal cliff, be prepared once again for extreme volatility. The VIX will probably have its day soon enough.

When there's volatility, investors seek safe haven.

And that safe haven, for investors and central banks alike, has been gold; just as it was during the last debt ceiling debate. This time, however, add in a layer of fiscal cliff.

Gold and Silver to Breakout

Gold futures prices lost more than 2% for the week and hit a two-month low on Friday in London; it was the fourth consecutive weekly decline.

The metal has now erased all its gains since the Fed announced QE3.

But as I mentioned in my Letter last week, and my Letter at the end of September, October is the worst month for gold:

"From a technical perspective, we still have some room to fall before gold moves back up on trend. There are few days before November officially starts and months end can often bring in intermediate lows. The recent drop in gold represents a great buying opportunity; possibly the last optimal intermediate buying opportunity for many months." October 28, 2012

"September is over and we're now heading into a month where gold has traditionally not performed as well. We've seen gold and silver prices rise over the last few weeks, so it wouldn't shock me that we see a pullback. October is also generally a more volatile month for both gold and stocks.

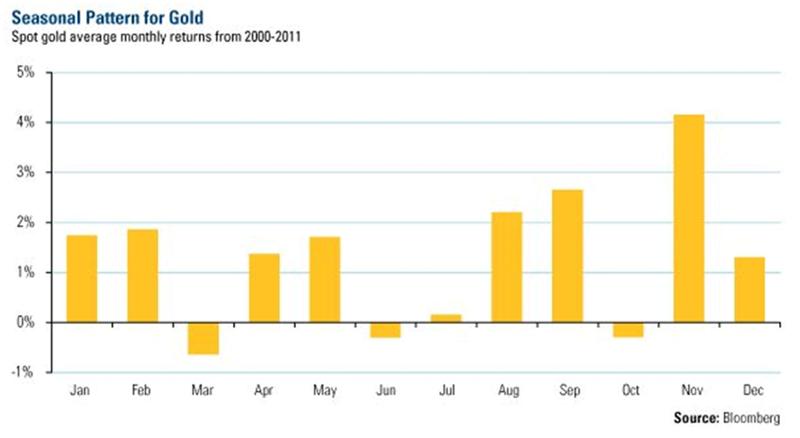

Should gold prices follow historical trends for October along with stocks, it would represent a great buying opportunity. Over the past 40 years, November has generally been one of the best months for gold, second only to September.

However, in the last decade, as seen in the (chart below), November has been the best performing month." September 30, 2012

Gold's strongest month for returns in the last 5, 10 years and 30 years is November - and by a significant margin.

As per Bloomberg's "Gold Seasonality Table," the 5 year average (2007-2011) saw returns of 5.6% and the 10 year average (2002-2011) saw returns of 5.1%

November's strongest gain over the 5 and 10 year period was the 12.9% gain seen in November 2008 - when President Obama was elected.

What will happen to gold if Obama gets re-elected next week, November continues to maintain its dominance as the best performing gold month, Greece goes back into the spotlight, Spain asks for another bailout, followed by the U.S. fiscal cliff and debt ceiling debates?

You'll see soon enough...

Gold and Silver Stocks to Climb

As I had mentioned last month in my letter, Watch the Throne:

"We have seen gold and silver stocks significantly outperform their metal counterparts. This trend should continue. Pullbacks in October represent a major buying opportunity in the sector - especially if gold follows the same trend as it has for the last 10 years."

The gold miners are already beginning to outperform both bullion and the S&P 500 and I expect this trend to continue given favorable fundamentals and seasonality. For the past six months, the silver miners and gold miners have outperformed.

This has been clearly shown in our own Equedia Select portfolio.

Equedia Selects Continue to Beat Market

Despite the dramatic drop in gold and silver prices last week, every one of our newly covered Equedia Select companies this year have hit new 52-week highs since our initial reports.

Last week, we witnessed great gains from almost all of them.

The mean average gain of all Equedia Select companies initially announced this year is 44% on the Canadian exchanges, and 46% on the American.

That means the current Equedia Select portfolio is beating the S&P, the Dow, the NASDAQ, the Gold Miners ETF (GDX), and the Gold Juniors ETF (GDXJ), and both gold and silver in the last 52 weeks:

Given the upcoming events of the Equedia Select companies and a potential precious metals rally in November, there's a good chance we could see them climb higher.

Timmins Gold (TSX: TMM) (NYSE MKT: TGD)

Timmins Gold continues to impress and outperform its peers. Take a look:

|

|

|

Source: RBC Capital Markets |

Next week, their Q3 earnings are scheduled to be released; as I mentioned in my original report, I expect it to be their best quarter ever - perhaps that's why buyside demand continues to storm into Timmins.

Last week, Timmins hit a new 52-week high of CDN$3.22 on the Canadian side, and US$3.24 on the American side on heavily traded volume.

That's a potential increase of 46% and 42% in share price from my initial report.

Initial Report: A Cash Flow Machine: Growing Gold Production with Significant Upside

Initial Report Share Price:

(TSX: TMM): $2.21

(NYSE MKT: TGD): $2.28

Current Share Price

(TSX: TMM): $3.00

(NYSE MKT: TGD): $3.01

Potential Gain: CDN36%, US32%

Highlight: New 52-week high of CDN $3.22 and $3.24 established last week

MAG Silver (TSX: MAG) (NYSE MKT: MVG)

MAG Silver also continues to impress, hitting a new 52-week high last week of CDN $13.13 on the Canadian exchange, and US$13.18 on the American.

That's a potential increase of 63% in share price from my initial report.

Initial Report: The World's Most Important Silver Project

Initial Report Share Price:

(TSX: MAG): $8.06

(NYSE MKT: MVG): $8.09

Current Share Price

(TSX: MAG): $12.94

(NYSE MKT: MVG): $13.00

Potential Gain: 61%

Highlight: New 52-week high of CDN $13.13 and US $13.18 established last week

Corvus Gold (TSX: KOR) (OTCQX: CORVF)

Corvus Gold also hit a new high, trading as high as CDN$1.70 on the Canadian exchange, and US$1.71 on the American; settling at CDN $1.57 and US$1.60 respectively.

That's a potential increase of 25% in share price from my initial report.

Initial Report: The Complete Package: A Massive Game Changer

Initial Report Share Price:

(TSX: KOR): $1.36

(OTCQX: CORVF): $1.37

Current Share Price

(TSX: KOR): $1.57

(OTCQX: CORVF): $1.60

Potential Gain: CDN15%, US17%

Highlight: All time high of CDN $1.70 and US $1.71 established last week

Balmoral Resources (TSX.V: BAR) (OTCQX: BALMF)

Balmoral has had tremendous success over the last few months and many of our subscribers have seen gains of well over 75% since our first report.

Even with the impressive exploration results, Balmoral has been stuck in the $0.94 range, as a result of the 12 million warrants at $0.94 set to expire on November 9. As a result, every time we see a move up higher, those with warrants are likely knocking it back down for some quick gains.

But by the end of next week on November 9, the warrant overhang will be gone and I wouldn't be surprised to see Balmoral trade higher as result; especially considering that the follow up holes on their recent new discovery and massive uncut hole of 273 g/t (8 oz/ton) Gold Over 3.88 Metres (12.7 Feet) continue to show us phenomenal grades (see last week's news release.)

Balmoral's management team continues to hit high grades and their drilling success just doesn`t seem to have an end. I expect that once the warrants expire, we may see higher share prices. Next week may be the last week of accumulation at these levels.

Initial Report: A Recipe for Success: One of the Biggest and Best Mining Packages

Initial Report Share Price:

(TSX.V: BAR): $0.57

(OTCQX: CORVF): $0.54

Current Share Price

(TSX.V: BAR): $0.94

(OTCQX: BALMF): $0.95

Potential Gain:

CDN 65%, US 76%

Highlight: Highs of CDN$1.10 and US$1.14 since initial report for a potential increase of 93% and 111% in share price.

Superstorm Sandy

For the first time in over 100 years, the stock market was closed for two consecutive days due to a weather related incident.

Those of you who have yet to see the destruction, estimated at well over $50b, should do a simple Google search: Sandy Storm Destruction

Once you do, you will get a better understanding of what our friends on the East Coast are going through. I want to wish everyone on the East Coast, and those with friends and family out there, the very best.

Keep in mind that New York state law allows for an extra day of voting if turnout is drastically suppressed because of a natural disaster like Superstorm Sandy. That could potentially postpone state, congressional and even presidential election results beyond Tuesday's Election Day.

Until next week,

Ivan Lo

Equedia Weekly