The report identifies five key areas of economic risk faced by Canada in particular, which I will summarize here. We begin with a brief analysis of global macrofinancial conditions and are immediately told that the Bank's economic outlook in all areas has been revised downwards significantly over the past six months. Europe is judged to be in a recession and recovery prospects in the US look bleak. The report points out that, amazingly, Canadian bank stocks are still trading at 70% above their book value, whereas US, UK and Euro bank stocks are well below this level. The Bank states that this is due to investors placing higher confidence in Canada's banking system, however if you've read my reports on the Canadian housing market (and look at the facts presented in this report) you might also come to the conclusion that much of the confidence is unfounded and could rapidly deteriorate as well.

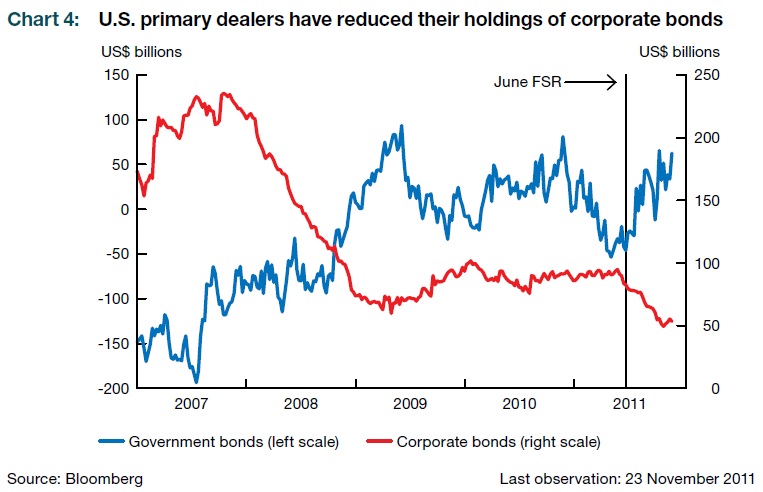

The report also confirms the statement made by many investment experts, such as Peter Schiff and here at TDV, that capital flight into government debt is crowding out private investment. This is part of what is prolonging the depression. Instead of financing economic recovery through investment in new ventures, projects and economic reorganization, primary dealers are instead simply financing the growth of government. This only further dampens the private economy and forms the vicious cycle that is sure to keep the economy in a recession.

As previously mentioned, the BoC identified five major areas of risk facing the global economy, which are as follows:

Global Sovereign Debt

It's somewhat telling that the BoC decided to list this first, as it illustrates just what a massive problem this is becoming. Tens of trillions have been invested in the debt of governments who are now facing massive budgetary and fiscal crises. An "adverse spiral" has been rated the principal threat to domestic financial stability and that this risk has already partly materialized. Incredibly, the BoC even considers the eventuality of the US dollar losing its reserve currency status:

"Until now, debt-service burdens in both [the USA and Japan] have been held down by favourable borrowing conditions - stemming in part from structural factors such as the high level of liquidity in the market for US Treasuries, the role of the US dollar as the international reserve currency and high domestic savings in Japan. There remains, however, a small but significant risk that this advantage could be lost if investor confidence suffers from repeated failure to undertake the needed fiscal consolidation."

Unsurprisingly, the BoC considers the numerous bailout and liquidity measures undertaken by central banks and the IMF to be "steps in the right direction" even though they specifically note that any relief that these measures provided was temporary at best and that the situation in Europe continues to deteriorate, with yields on sovereign debt moving sharply higher in a number of Eurozone members.

The chapter concludes that the debt crisis "can be resolved if policy-makers address the situation in a forceful manner... based on credible fiscal arrangements and enhanced governance." In other words, even more government involvement in the financial system. This has already proven to be useless, as the BoC admitted in an earlier segment of this chapter so one has to ask why they believe that more of the same is necessary.

Economic Downturn in Advanced Economies

In the next risk, the BoC notes what everyone should now be aware of; global economic activity is slowing down markedly. Household and bank deleveraging is dragging the world economy deeper into recession. Further downturns in advanced economies would have a substantial impact on Canadian businesses, households and financial institutions transmitted through bank losses and deteriorating credit quality. The BoC notes that while some banks have increased their capital buffers other banks still have razor-thin cushions and high exposures to underperforming assets. The obvious conclusion we should reach from this is that there continues to be massive, systemic risks in the financial system that could send waves of destruction throughout the global economy.

There are also concerns over asset quality for the global banking sector. The report notes that the US real estate market is vulnerable to further deterioration and that stagnant wage growth is impairing the ability of borrowers to service their mortgage debt. A massive overhang in the supply of housing also persists. Banks have foreclosed on a large number of properties and are unable to liquidate them at what the BoC calls "reasonable prices". Unbeknownst to the BoC, a reasonable price would be one where buyers would be willing to buy. The fact that banks possess this huge stock of houses actually indicates that they're asking unreasonable prices for them. Non-performing loans in the UK and Eurozone are at nearly 7% of total loans and climbing. In the US these loans now represent about 2.3%, down from a high of about 3.5% in 2009, and in Canada it is at about 1% of total loans and showing a small decline since 2010. Despite Canada's low levels, the Bank concludes that:

"If economic activity declines significantly, a growing number of Canadian households and businesses would experience financial difficulties, which would translate into an increase in loan losses at financial institutions. If banks curtail credit, this would trigger an adverse feedback loop through which declines in economic activity and stress in the financial system would reinforce each other."

This statement mirrors what I had predicted in my article "